Tag: Financial Literacy

Financial Education through Real Estate Investing — Complete your Wheel of Wealth for a Smooth Financial Journey (Part 2/2)

April 12, 2022

First off, I want to share a quick example on WHY understanding the Wheel of Wealth is so vitally important for anyone who wants to go PRO in the world of real estate investing.

I have worked with many students that were worth so much more than me when they come to me for help. They’ve simply done really well by following the basics: get good jobs, make high incomes, control expenses and buy properties. Properties that initially never cash flowed until market rents caught up. Even then, the cash flow amounts were pathetic (their word, not mine) because they were waiting for the big cash out once the mortgages are fully paid down…in 20, 25 or 30 years.

Very quickly, through one on one discussions and seeing how they handle opportunities that come their way, it’s ‘habitual’ for them to just ‘buy’. These also tend to be the people that have told me “somedays, I/we feel like slaves to our jobs, our properties AND our tenants. We pay them to be there because we don’t make any money until the very end.” They have this uncontrollable need to BUY and COLLECT. Before you know it, two, three and maybe even four decades have gone by. That’s great if that’s what you’d like and are able to put up with decades of stress like that. These are the people (I really don’t call them investors) that only feed into 2 buckets still: earned and portfolio. To me, those are the two income buckets that any average person has been taught to do growing up as discussed in Part 1. This is interesting to me because it’s like putting a driving coach in a car with someone who’s been driving for 20 years. Even with a good clean driving records, the driving coach can typically pick out “bad habits” that are blind spots to the long-time driver within seconds.

For many, it’s about rewiring our thought process and financial blueprint. Again, don’t get me wrong, there’s nothing bad about retiring with a buttload of portfolio income. It’s just that, one of my mentors in my early days asked me this question that really stopped me cold: do you want to be young and rich or old and rich? The key word here is not rich. It’s TIME.

The concept of time needs to be the first concept for all investors to learn and fully comprehend before anything else matters.

Onthat note, let’s come back and look at the hard and soft strategies again first:

- Distressed Properties & Flip (physical buy and sell of a property)

- Wholesale & Assignment (paper buy and sell of a property)

- Lease Options (physical or paper buy and sell of a property)

- Short-Term Rentals: vacation, executive, student and rooming houses

- Private Lending & Creative Financing

- Income Properties: single family

- Income Properties: multi-unit residential

- Income Properties: commercial, mixed use and industrial

- Infills and Land Development

- Asset & Income Protection

- Business Fundamentals: business planning & goal setting, bookkeeping, systemization, networking, etc.

- Portfolio Management: tenant management & management of the physical asset

- Raising Capital

- Creative Financing: small to large scale partnerships

Frankly, this list is not exhaustive, yet. In different countries/jurisdictions, there are many more available. However, for the sake of demonstrating the concept, we’ll keep this list for now.

From this point forward, typically we have 2 main steps on how to complete the Wheel of Wealth with the 14 listed strategies:

First — understand which income bucket each strategy goes into, and

Second — understand how to use it to our advantage to accomplish our financial goals.

Distressed Properties & Flip (physical buy and sell of a property)

This hard strategy falls under earned income for most especially when the clear ‘exit’ is to sell it once the value-add process is done. However, one thing to note is that distressed properties really is the foundational strategy of all property-first deals. As a result, many people have heard of the BRRRR process. BRRRR stands for Buy, Renovate, Rent, Refinance, and Repeat. It’s also important to know that BRRRR is NOT a strategy in itself as we BRRRR all property types (even businesses!). Amateurs who want to sound fancy will often times refer to this as a strategy. Please do not sound like one after reading this article — you’re better than that 🙂

I would personally put this strategy in all 3 income buckets if the exit strategy isn’t to sell immediately after the value-add (aka renovation) is done. Why? Because of one very crucial thing pointed out earlier — it is the foundational strategy of all property-first deals. Whether it’s a small single family, a 12-unit apartment building or 1,000-unit apartment building complex (or even commercial and industrial units), you will BRRRR them. And when you decide to keep them for cashflow, you now have passive and portfolio income for the long haul. While not directly in the passive and portfolio income buckets, it definitely is a main contributor for both.

Wholesale & Assignment (paper buy and sell of a property)

This hard strategy falls under the earned income bucket. Simple. Be the personal shopper in the real estate investing industry is what I call a wholesaler — doesn’t that sound fun?!

Lease Options (physical or paper buy and sell of a property)

Oh boy, this one is gonna be fun. Like distressed properties, this one contributes to all 3 — earned, passive and portfolio — income buckets. Unlike distressed properties, it can do it in a very direct ways. It’s worth noting that lease options can be used as both acquisition and exit strategies in real estate transactions. Frankly, for my readers who do day trading, you simply don’t need anymore explanation on this one.

Short-Term Rentals (STRs): vacation, executive, student and rooming houses

Definition matters in the world of investing. How we define short-term rentals is simply by the length of a typical tenancy which is 12 months. STRs can be either earned OR passive+portfolio income depending on one main factor: are you the active manager dealing with your tenants and bookings? If you are, then it’s likely an earned income bucket strategy for you. If you are hiring out the day-to-day management, then it’s simply passive+portfolio on properties that you have in your portfolio.

Private Lending & Creative Financing

First thing first, if you’re not licensed to trade in loans and mortgages, tread carefully on how you allocate this strategy into your income buckets. For example, mortgage brokers are legally licensed to trade in loans and mortgages. Most private investors aren’t. Amongst your close circles, you are able to leverage this strategy and feed all 3 — earned, passive and portfolio — income buckets. Certain creative financing methods will feed into your passive+portfolio income buckets only.

Income Properties — all kinds

Income Properties, by definition, is making you income every month so it definitely checks off the passive income bucket box. However, when done right and well, all income properties should feed into your portfolio income bucket as well. There are certain formula and key performance indicators as our north star to make sure both buckets are fed properly. Otherwise, we are no better than the example in the opening story.

Infills & Development

Perhaps the strategy that has the widest spectrum as you can build whatever you want here! Once again, to keep things simple, infills and development is what I would describe as distressed properties on mega steroids (except that maybe there isn’t an actual piece of dwelling sitting on the land sometimes and it’s just…land). As a result, if you sell it once it’s built, it’s definitely goes into your earned income bucket. If you hold on to it, it turns into an income property and thus feeding into your passive and portfolio income buckets.

Taking a turn here, ALL soft strategies go into all 3 income buckets. That makes it easy. Whew!

Now that we’ve gone through that, let’s make it a bit more relevant and start speaking everyday English, shall we?

Let’s say: if your why for investing is because you’d like to —

- Have better vacations with the fam every year

- Your job is “stable” — meaning your hours and stress levels and earning potential are predictable and capped

- You want to pick up a lucrative side hustle without the extra tax bills

You might be perfect for a mixture of distressed properties & flip, wholesale & assignment, and lease options.

Let’s say: if your why for investing is because you’d like to —

- Secure your retirement because, frankly, every time you look at your quarterly statements from whatever it is your money is in, you lose a few nights of sleep

- Make sure you don’t become 100% dependent on the government or, worse yet, become a burden to your children

You might be perfect for a mixture of lease options, income properties (types of property dependent upon your personal risk tolerance) and private lending & creative financing.

Let’s say: if your why for investing is because you’d like to —

- Have time and money freedom and enough to fire your boss one day (date TBD)

- Build and live a life by design and with purpose

You might be perfect for a mixture of lease options, income properties, STRs, private lending & creative financing.

Of course, there are many ‘it depends’ in every scenario. However, I hope that the essence of the thought process here is captured and understood.

Toconclude the whole concept of WHY it’s important to understand and complete your own Wheel of Wealth: you will never have to ask which market(s) to go into ever again. One of my mentors said this to me: build your own wheel so you never have to chase markets. Across the world right now, changes are happening everywhere — rising interest rates, governments capping rent increases, higher than ever before-seen property values, highest inflation rate and climbing every quarter, etc. Change is the only constant. When you round out your own Wheel, you never have to worry about what the market is doing. For instance, we started building (infill & development) in 2017 long before the amateurs are flocking into developing new properties because they just learned that there’s an overall shortage of housing in the country. I learned that when I was building my passive income, there were already people developing. And that precisely IS the point here: we are all at different stages of our wealth creation plan. When you have built yourself a safety net, it doesn’t matter what’s happening to the world. You’re financially independent and free first before you take on more (calculated) risk.

Inthe next article, I will share with our personal investing philosophy and, more importantly, process. It has been my guiding light for the last 7 years. Yes, 7 out of the 12 years since I started learning and applying because I finally figured out a formula that can be duplicated. A formula that will compliment the Wheel of Wealth and has the potential completely alter how you look at real estate as an investment tool.

For my dedicated readers, I thank you for your support and feedback. If this is the first time you’re reading one of my publications, I hope you’ve enjoyed it and learned a thing or two.

For those of you who prefer watching videos, here is the YouTube channel where some of my work (very raw) has been shared.

Financial Education through Real Estate Investing — The SMP Philosophy

April 19, 2022

This one is arguably the ‘giving away the farm’, the ‘secret sauce’, and the ‘peek behind the curtain’ of how I’ve been able and continue to create the financial results today. It’s simple and yet not easy to hold onto (full disclosure here). It’s also one that’s central to all of Trust Your Talent Academy’s training curriculum. It’s a process, a formula, a mantra or simply my investing philosophy. And it is proprietary.

This process has been my guiding light for the last 7 years (since ~2015). Yes, 7 out of the 12 years since I started learning how to become a professional investor in real estate. Like some, I jumped in once I started learning about the different strategies. Lease Options, in particular, is one that provided me with the initial financial freedom I was looking for. Unlike many, I wanted to make sure that my new found “time & money freedom” is one that lasts. So, every step of the way, I looked for patterns and methods to create systems that are duplicatable.

1st SMP = Strategy — Market — Property.

And yes, in that exact order.

A strategy for an investor is a way to determine how we make money and how much money we make BEFORE we get into any deals. Read that again.

That is the whole point of why someone wants to start investing wisely and ‘strategically’. First of all — having a strategy contributes directly to your income and financial goals. It is, after all, why you are even reading these articles in the first place— to create and gain more financial resources to build the life that you want and deserve. Secondly, having the right strategies is like having the right tools — you get things built much more effectively and efficiently. Time is everything as we’ve discussed in the past.

From the Wheel of Wealth, we’ve learned some of the currently available and popular strategies that real estate investors use (in North America). Those strategies are only meaningful and USEFUL when your ‘why’ has been translated into goals, and those goals translated into a money figure. Now, it’s time to let your properly determined goals decide the strategies you should embark on.

For example, my goal was to quit my corporate job within 3 years so that I could free up the time to take care of my health, and later create a “career” that I would love and not have my livelihood depend on it. As a result, I chose Lease Options as my first strategy to focus on given the assessed resources I had at the time during my first mentorship with a real estate investing mentor. From my 1st class (January 2010) to the day I declared financial freedom (July 25, 2012), I focused on only this one strategy.

Calling Edmonton, Alberta home had its advantages at the time because I was able to leverage this strategy right in my home market. Although it’s not a must nor does it provide the best return, after an exhaustive process of listing pros and cons and market selections, that’s what we decided would make the most sense.

Then we would look at the properties that would support this strategy.

And there you have it:

Strategy(-ies): Lease Options (tenant-first)

Market(s): Edmonton & surrounding areas, AB

Property(-ies) Type: Single Family Home

The reason why this process is so powerful is because it’s pretty much the exact opposite of how most amateurs or real estate investor wanna-bes operate. It’s what we’d call the Buy Rent & Pray. The most successful investors of our time, Warren Buffet, is famous for his contrarian way of making investing decisions. In essence, do the opposite of what the majority is doing strategically and we can all create financial successes in life.

Let’s quickly break down the Buy Rent & Pray process so that you are clear about WHAT NOT TO DO:

BUY —

Inevitably, you have to acquire properties to make money from them, right?! In short, yes. However, it depends on how you define ‘buying’ in this case. We will cover that in another article down the road. For now, we’ll look at the behaviours amateurs exhibit during the buy part of this process:

- Get onto realtors’ mailing lists (likely in their home market) and attend open houses to look for properties. These properties are probably within their affordability. They also tend to be emotionally involved in the buying process or easily swayed on what to buy just “to get into the market”.

- Sign up for alerts on pre-construction from developers. These properties are likely within their affordability. And they are convinced that the property value has nowhere to go but up.

- Join investing clubs or conferences and get lots of ideas and opportunities about properties and markets. These ‘ideas and opportunities’ tend to support the amateur’s existing confirmation bias. This is an interesting one for me personally. To me, it’s like joining the alumni association without every attending the school prior. It’s buying an expensive country club membership without ever learning how to swing a golf club properly. It’s also like wanting to build a bridge with a marketing degree (that was my degree).

Don’t get me wrong, I’m not saying any of the above 3 things are bad. I’m just saying that they are a BAD FIRST STEP in the process of leveraging real estate investing to create financial wellness — in both the short- and long-term.

RENT —

Once the property’s acquired, here’s generally what happens:

- Do the advertising and start showing the property to potential tenants.

- Take the time to do showings. Most of the times amateurs will self manage because it’s in their home market to save some money. That right there is symptomatic and against the fundamental investor mindset. An investor is one that focuses on ‘how much is it going to make me’ vs ‘how much is it going to cost me’ — this spells the ROI (return on investment) mindset.

- Overestimate revenue and underestimate budgets because they either didn’t know how to do a proper deal analysis or misguided by the wrong people who just wanted to sell them the property in the first place.

PRAY —

Forget about the first 2 steps for a while. This is really the focus of this process for many amateurs. Now that they’ve acquired the property and rented it out, they simply pray that:

- The tenants always pay rent on time and don’t cause troubles;

- The tenants always take care of the property well;

- The physical asset (aka the property itself) doesn’t have too many defects and issues over time that will call for a lot of time, money and energy to fix.

In the perfect world, this process could work. In the perfect world.

Professional and educated investors take calculated risks. Again, investing inherently has risks. All we are doing here is arming ourselves with the tools and strategies to:

- Predetermine the viability of every deal and the range of profit we will make BEFORE committing to the ‘purchase; and

- Have multiple exit strategies should we choose to exit them and move on for whatever reason.

Side note: notice how I said ‘for whatever reason’? That’s because I’ve attended countless real estate investing courses and meet-ups over the years and one of the common ‘regrets’ I hear people say is this: I regret selling my properties. What is so bad with that? For starters, properties are like people. The older we get, the costlier it gets to maintain. From a financial performance standpoint, it typically means that the profit level goes down at the year goes by regardless of how much equity has been built. Like people, there’s no point being the wealthiest person in a cemetery. There’s also little to no point having a portfolio with the most equity. Also, with the highest inflation rate in 40+ years, money is devaluing faster than usual. True financial education in real estate investing means that your money needs to at least outrun inflation. Unfortunately, most amateur investors weren’t taught to think that way. And, to be honest, I didn’t in the beginning either.

So, here’s the difference with my personal and initial SMP:

Strategy: Lease Options (tenant-first)

I know that I will cashflow from Day 1 once I’ve acquire the property (or within a few short days of possession). I know that an average deal will cashflow $800-$1,200 per month before I even make an offer on a property. There’s no guessing here when the proper steps are carried out. By the way, how many of these deals do you need to not have to worry about life expenses?

Market: Edmonton & surrounding areas, AB

I know that this market has a lot of the right tenants (we actually call them tenant-buyers in this case) that can use the help through this strategy to become homeowners as they’ve dreamed and planned for. The market itself also provides a healthy range of options in price that make sense for the end buyers.

Property Type: Single Family Home

I know that this is what most people (tenant-buyers) want to get into so the demand is there. “We buy for demand” vs “we buy properties” is also another way to look at it.

One of my favourite quotes by Zig Ziglar is this:

This strategy not only contributed to my personal goal, but, better yet, can create such a positive impact in so many people’s lives.

2nd SMP = Support — Mentorship — Program/Steps.

This one is much more comprehensive and serves as an ingredient list for sustainable success in all areas. However, since we are focusing on financial education through real estate investing, this is how we’re going to use it.

Having support from like-minded people is HUGE especially when you’ve had zero role model in your life who has achieved what you want to achieve. Knowing that there are others (while not many) out there yearning for the same thing (better life standards, more resources, less financial stress) and are on the same journey is invaluable. A community like that is one of the key ingredients.

Mentorships in life for most of us happen from the day we’re born. Our parents (at least the ‘good’ ones) are our first set of mentors. However, a mentor really is someone who not only wants the best for you, but have already achieved what you want to achieve so that they can show you the way. I remember how against it my parents were when I asked them to support some of my tuition in financial education (remember I had just lost my life savings when I discovered financial education through real estate infesting?). They promptly rejected the idea and my ask. Instead, they offered for me to go back to get my MBA (Masters of Business Administration) and they would be happy to go into more debt to pay for that. I had to quickly get a hold of my own frustration and remind myself to look at the situation objectively. My parents, middle middle-class at best at the time, are telling me not to get educated to create a better financial future for myself. What? That seems to go against everything they’ve taught me and wanted for me. Then I realize that it’s because they don’t know what they don’t know. There’s no disrespect here because that is the simple truth. Fortunately, once I made up my mind that I was going to have a mentor (and many more as I grew as a person, as an investor and as a mentor to others) to help me, all that frustration and anger just subsides.

Program/Steps. “Success leaves clues.” This is why we often see people joining programs and follow the steps to achieve certain results we want. Be it physical health or financial health, the concept is the same. While not all programs are created equally even for financial education, it’s important to know that this is a core ingredient for success.

For my dedicated readers, I thank you for your support and feedback. If this is the first time you’re reading one of my publications, I hope you’ve enjoyed it and learned a thing or two.

For those of you who prefer watching videos, here is the YouTube channel where some of my work (very raw) has been shared.

(Written at the Four Seasons Whistler Residences)

Financial Education: Know the Difference — Cash on Cash Return vs Return on Investment

May 3, 2022

Imust confess. To this day, I still have a hard time walking into a Walmart , any Walmart— for a few different reasons. One of them is knowing that most of these greeters don’t ‘choose’ to work. They still have to work and most of them are seniors. In the rare times that I do, for some weird reason, I have Warren Buffett talking in my ear: “if you don’t find a way to make money while you sleep, you will work until the day you die.” Truthfully, I don’t have any qualms about the latter part as long as I love doing what I love every single day. Even if it’s considered work.

Learning how to invest and financial education has been an incredibly fun and rewarding journey so far. And I’m still learning everyday. It’s almost as if the more I learn, the less I know. And for a while now, that’s ok. I’m no longer worried about not getting 100% at a test and getting scolded. Or, worse yet, getting questioned on how much effort I’ve put into my work. I know that , if I’ve given what I want to do 100% of everything I got right now, I’m ok with the outcome — whatever it may be. If the outcome is not ideal, it simply means that I need an adjustment or improvement somewhere. In mindset, in knowledge level or in my skill level.

What does that have anything to do with this topic, you ask? Simple. And here’s the thought process:

- Most of us have the tendency to work harder when we want ‘more’. More money to be specifically.

- Investing is learning how money works for itself.

- Many people and ‘investors’ (I will use that term loosely here), once they acquire a property, it’s like set and forget. It’s likely one of the worse things to do as an educated investor.

- The calculations of ‘returns’ on investment deals is an important process. And the numbers represents how hard our money is working for us.

If we are willing to work hard, why wouldn’t we make sure our money works harder than us?

The answer to this question, as I’ve witnessed over the years, has separated people who just added long-term wealth (through inflation mostly) and people who achieve sustainable financial freedom.

Many ‘investors’ and sales people in the financial planning industries seem to use these terms incorrectly and interchangeably. Understanding the difference between the two terms have helped me in making buying and selling decisions of real estate investment deals more effectively and efficiently. After all, it’s all about making sure our money is working hard(er) for us so we can free up more time and energy (and money) to pursue the things we really want to do.

What is Cash on Cash Return (CoC)

Dictionary.com defines cash-on-cash return as…wait, wait, wait! Don’t go yet. I’m just kidding! Like a Best Man’s speech that nobody wants to listen to, I’m not about to take that approach…yet. However, acknowledging that I’t know everything, I may have borrow some definitions from time to time to prove a point.

I will say this though: my favourite ‘dictionary’ these days is www.Investopedia.com when I learn a new term related to investing or money. So, guess what, Investopedia defines “A cash-on-cash return [as] a rate of return often used in real estate transactions that calculates the cash income earned on the cash invested in a property.” It would be good to note that this refers to pre-tax income.

However, the way I learned it is simply this: the CoC is basically like the interest rate you earn. For example: if the bank is promising you 2% a year (year right 😅…) on your money in a savings account. Your CoC is 2%. Of course, if we were to get a bit more technical, then this typically would refer to simple interest.

As a result, CoC is commonly used in any sort of income properties — single family, multi-unit residential, commercial, serviced accommodations, etc. In addition, many private lending deals are dealt in simple interest so the interest rate offered by the lender (or borrower) is a directly CoC return — not counting any additional fees the lenders may impose.

CoC is a straightforward and simple measuring stick for us to know how hard our money is working for us on an annual basis. This really should serve as an indicator for investors who understands fundamentally how to leverage real estate as an investment tool. When the CoC goes down (and it typically does) to a certain point, it may be time to ‘trade up’. At this point, there’s usually some equity built up as well.

What is Return on Investment (ROI)

On the other hand, ROI is a way to measure the overall investment performance when there’s a clear start and a clear end. To compare apples to apples and borrowing Investopedia’s definition: Return on investment (ROI) is a performance measure used to evaluate the efficiency or profitability of an investment or compare the efficiency of a number of different investments.

As a result, ROI is typically tied directly with strategies like Flips and Lease Options. These strategies are known to have clear start and end dates.

Just like not all deals and not all strategies are created equally, these two terms also aren’t. They exist for a reason. To me, the reason is to support us in making better and faster decisions when searching for and comparing deals at hand.

The lesson here remains: real estate is just our vehicle in investing. The goal is to create better financial resources and blueprints for ourselves, and hopefully generations to come. Making sure our money is working hard for us at all time is, in my opinion, the highest level of the art of investing.

If you’re intrigued by this article, I would also suggest a topic for you to dig deeper into also: the velocity of money. You can read up on it or watch videos.

Tomy dedicated readers, I thank you for your support and feedback. If this is the first time you’re reading one of my publications, I hope you’ve enjoyed it and learned a thing or two.

For those of you who prefer watching videos, here is the YouTube channel where some of my work (very raw) has been shared.

(Written at home in Edmonton, AB)

Financial Education through Real Estate: How to Choose a REI Mentor (Part 1/2 — Top 3 Qualities)

May 10, 2022

Truly, the best part about what I get to do these days is share my education and experiences with others who have the same goal of achieving financial freedom (and didn’t think it was possible or attainable) as when I first started going down the path less traveled.

When this journey officially began in 2010, I remember sitting in a hotel ballroom during my initial Bootcamp weekend. While learning the foundation of how to leverage real estate investing strategies to create a high performing portfolio that would contribute to my personal goal of financial freedom, I was also inspired by the trainer that weekend. At one point, I turned to my husband, pointing at the trainer on stage, and said: “one day, I want to be just like him.” His level of energy, positivity and the idea that we live in a world of abundance — more specifically, financial abundance — was not only inspiring, but refreshing. I felt like my soul was cleansed and any negative views and unkind ideas about money that I grew up with started to vanish that weekend.

In 2014, my dream came true. This was a dream because I actually didn’t set a deadline for it so it wasn’t a goal (definitions matter sometimes, remember?!).

Since declaring our own financial freedom on July 25, 2012 (and I hope to hear your date at some point), I continue to build our portfolio. However, admittedly, I started getting ‘bored’. Yes, as a 30-year-old, it was my egotistic way of wanting more challenges in life. Yet, the idea of doing anything else (ie. working for someone else) seemed unappealing and, quite frankly, a little idiotic. After all, didn’t I just bust my ass off for the last 2 years — learning and applying and building my portfolio — so I wouldn’t have to do that again?

My “better half” had the foresight. He continued to stay employed. And if you asked, he would tell you that he was simply following the trainer’s suggestion: when you are financially free, it can simply mean that you work because you want to, not because you have to. You work because the work you choose to do can now serve a purpose — whatever that is to you. He wanted to stay employed to further his skills and because he loves the social environment. It certainly didn’t hurt that he always learned fast, excelled at what he did and most of his pay checks reflected his effort.

I, on the other hand, had to really battle through that idea. This is also one of the reasons why I continue to say: I’m not the smartest person in the room ever! And, I pray that I don’t ever put myself in a room like that. Growth is so vitally important to my very being today. This has become the reason why I believe in the concept and active engagement of mentorship (of any kind) with all my given and earned wisdom to date.

In this article, I share the top 3 qualities that I look for on how to choose a mentor for you in your real estate investing journey. They are the combined perspectives of myself being a mentee many times in the last 12+ years and a mentor in the last 8.

The Top 3 Qualities I look for in a real estate investing Mentor:

1. They have achieved what I want to achieve.

This ‘quality’ is twofold: One — as the title suggested: they have paved the way for me to follow to create the results I want for myself. Two — it helps me collapse my timeframe. The latter is definitely the more important factor. Even to this day, whenever I get the chance to teach a Financial Education Bootcamp (we view this as the foundation for building a successful and sustainable real estate portfolio), I always ask people to complete this sentence: Time is _______. Unsurprisingly, almost without exception, 100% of the times, that blank is filled in with the word money. When, in fact, looking at time closely, TIME is EVERYTHING! These are 2 of my favourite quotes about time that I’d like to share:

When you ask around to see if anyone’s invested in a mentor in their lives, you’ll find out that the answer is most likely yes —

Yes to having a dance tutor.

Yes to having a piano teacher.

Yes to having a football coach.

Yes to having a personal trainer.

Yes to having a personal growth coach.

Yes to having a mentor in pursuit of higher education and degrees.

The list goes on. Aside from any natural notion of ‘going with the flow’ at any age or for whatever reason (I’ve been told that having a designated mentor when you’re getting a PhD is a must), most would say that these are conscious and welcoming decisions they happily made.

The mentors get to share their knowledge and experience, and we get to drink it all up like a jello shot at a party! Ok, maybe not the best analogy, but I think you get the idea. It’s easy, fun and the effect is often quite immediate.

With that said, the SMP Philosophy has applied quite well for everyone on this journey. I stand for leveraging real estate investing strategies to achieve financial freedom because that was my goal and is my passion. I know some others may choose a mentor based on a single strategy, a market or a certain type of property. The importance is that you and your potential mentor align on your goal.

2. They have my best interest at heart.

Itgoes without saying that life can be difficult and downright sucky at times. During those times, the comfort and solace we find in a bear hug from our loved ones, or maybe even just some consoling words may be what we crave the most. Yet, is it what we need the most?

Even with goal alignment, I want a mentor who is unapologetically straight with me. After all, my FIRST reason to have a mentor is to grow, and in ways that I may not even know I’m capable of (read that last line again). For example:

- When I am stuck, they guide me through the thought process rather than just giving me the answer. They want me to truly learn how to fish so I can eat for life rather than giving me a fish right now. However, rest assured, they are there to cheer me on and holding my hands when I’m wobbly in the process.

- They tell me what I need to hear and not what I want to hear (even if it’s hard for them to say). I’m fully aware of the fact that they are not here as my friends (at first). We are not buddies (at first). This is all with the purpose to help me grow. I grew up in Taiwan and had plenty of experiences of “teachers” yelling at and beating me (physically — yes, I’m from that era and that culture). The tough love is DEFINITELY NEEDED sometimes even as a grown man. A long-term friendship may develop organically over time but it’s not the focus.

- They don’t give up on me as long as I’m showing effort. This one probably hits home for me the most especially after the last point. As a real estate investing mentor for just over 8 years now for people from around the world, I can proudly say that I have NEVER missed anyone’s effort to stay connected and to get reconnected when they needed help — regardless of how long it’s been. However, I do make it very clear that the premise is “as long as they are making an effort” to learn and grow. I’ve simply come to embrace the fact that both timing and time are equally important. Having benefited from rebuilding long lost relationships (or just the ones that maybe got parked because life took a detour), I believe that this relationship is no different. One of my favourite quotes is this:

I’ve learned a few lessons the hard way over the years: “you can’t help those who don’t want to be helped” and “people don’t place value on something they get for free”. As much as I wholeheartedly believe that EVERYONE can achieve financial freedom, I’ve encountered, countless times, folks who don’t want it as badly as I want it for them. It’s simply not going to work. This is where also I would personally appreciate getting rejected by a potential mentor. They’re basically just telling me that I’m not ready to receive yet.

3. They are open about their failures.

Ipersonally LOVE the word “failure” — now. Growing up, failing meant a stern talk if not full out scolding was in the near future. That is, if I was lucky enough to not get beat when my test results were bad. Failing also meant looking bad. And I believe we all learned this lesson over and over again from our upbringings all the way to our day-to-day life now, too.

Failure is a blessing. Failure is a stepping stone. Failure is success in progress. As mentioned in Part 2 of Mindset, losing $1M overnight by far is the biggest failure I’ve had to work through. However, without it, I wouldn’t have come back stronger and better, doubled my portfolio and tripled my passive income in half the time compared to the first time around, and found the courage to start Trust Your Talent Academy to make sure as many people as possible can learn to avoid the mistakes that I’ve made. Not only that, I’ve been told that one of my opening lines when I teach has been: “You are really all here to learn the collective lessons of what not to do from me and the investors that have also come before me in real estate investing.” After all, as one of my mentors put it: “You can make a lot of money in real estate investing if you know what you’re doing. And you can lose a lot of money in real estate investing if you don’t know what you’re doing.”

I know what we are teaching and how we’re guiding new and seasoned investors holds one of the core values at Trust Your Talent: sustainability. Staying power matters. Those who continue to bust through and learn from setbacks are the ones in it for the long haul. After all, a life without having to worry about financial issues is freeing and rewarding.

Here is a quick video that has inspired me for years and I’d love to share it with you: Famous Failures.

This is a topic that I can go on sharing forever — both as a mentee and a mentor. As evident as it may be, I will risk sounding like a broken record here. Everyone needs a (if not multiple) mentor on their real estate investing journey. Based on the SMP Philosophy, I’ve had many mentors in my journey so far and I know it will continue to be that way.

In the next article, I will also share some of my personal experiences with some of the qualities that are definitely deal breakers — meaning, even if you ‘mentor’ me for free, I wouldn’t take it.

Tomy dedicated readers, I thank you for your support and feedback. If this is the first time you’re reading one of my publications, I hope you’ve enjoyed it and learned a thing or two.

If you’re wanting to be a part of a community of real estate investors from around the globe, here is the T.A.L.E.N.T.ed Investors Facebook Group. It’s a place where people come together to share experiences, knowledge, successes and challenges, and money making opportunities!

For those of you who prefer watching videos, here is the YouTube channel where some of my work (very raw) has been shared.

(Written at home in Edmonton, AB)

Financial Education through Real Estate — How to Choose a REI Mentor (Part 1.5/2 — Top 3 Deal Breakers)

May 17, 2020

(WARNING: COLOURFUL LANGUAGE IN CONTENT)

This one is the hardest piece I have had to write to date. Like most experienced investors who have gone through the ups and downs building their portfolios, overtime our ‘what not to do’ list is actually much bigger than the ‘what to do’ one. This is done all in the hopes that the deal quality gets better and better. I joke with full truth a lot about this: if your first deal is your best deal, you’re doing it wrong! So…without going into too much of a tangent, here’s part 1.5/2 on the top 3 deal breakers for me when choosing a REI mentor these days.

For the record, I have a very deep appreciation for those brave enough to offer any kind of real estate investing training these days. Real estate, while being the most tried and tested asset class in human history, is also a moody animal. Training people on real estate investing can sometimes feel like training people on lion taming. Moreover, I also share the utmost respect for anyone courageous enough to offer financial education. It’s definitely the path less travelled. And, the mission of “creating financial independence one person at a time” is definitely one that requires more than just Trust Your Talent can accomplish. For that, I am grateful that there are others in the same industry.

On that note, it would be prudent to define what ‘industry’ that I am/we are in for doing what I get to do everyday. Like the titles of all of my published articles on this platform so far have suggested: financial education or financial education through real estate investing. Often times, people ask me about ‘competition’ in our industry and in the marketplace, my reaction has always been: there really aren’t that many — globally. Fortunately, I always say that “results always speak louder than words”. Usually, when people get to meet someone from and/or trained by Trust Your Talent, the question answers itself.

With that frame of mind, here’s my list of the top 3 deal breakers when choosing my next REI mentor:

To begin, borrowing from the previous article:

I stand for leveraging real estate investing strategies to achieve financial freedom because that was my goal and is my passion. I know some others may choose a mentor based on a single strategy, a market or a certain type of property. The importance is that you and your potential mentor align on your goal.

1. Misalignment in vision

For me, the purpose of putting my work and journey out there from day 1 is first and foremost to help others create financial independence or financial freedom through financial education. (Side note: it’s very uncomfortable to share a lot of the things I’ve been sharing. However, my mentor did tell me that I’d have to face my own fears and focus on the bigger picture. So here I am, stepping out of my comfort zone.).

What financial education has done for me is beyond what I could comprehend some days still. Yet, I feel it in my bones everyday that more people need to at least hear about it, if not allow themselves to start on it. Exemplified by one of my favourite quotes here, while traditional school (with a very pricey tag to my somewhat middle-class parents) bought me a poor mindset, a major clinical depression and my 3rd heart attack; financial education bought me time and money freedom, and later on, the ability to execute on my personal vision to help others achieve the same.

Ever since the first Wheel of Wealth article was shared, I’ve gotten very encouraging feedback from many of my readers. Perhaps it’s because it struck a chord — whether you’re a new grad from college/university, a highly trained professional (MD/PhD, engineer, accountant, nurse, marketer, programmer, etc.) or have simply fallen into the rat race.

As mentioned in the SMP Philosophy, it wasn’t always around when I first started learning and applying as an educated investor. It took time, more mentorship and further knowledge to distill the process. I firmly believe that if you don’t know where you are going, you’ll end up where you don’t want to be. Investing is very much like that. Over the years, I’ve seen people acquire properties and grow their portfolios only to end up with a 2nd job. It was shocking at first. However, when I dug deeper into these people’s stories, it was unsurprising to see how they end up where they are despite having numerous rental properties. Like one of those singing competition shows, it’s a constant balance between advancing one week at a time and still with a clear end goal in mind. I have hardly come across people admitting wearing the name badge of a Real Estate Investor that go into it with the goal to add more stress and to-do lists to their plate. Yet, so many do.

I, myself, and the creation of Trust Your Talent stand for the ideology of total wellness. This ideology is composed with wellnesses in 5 major areas in our daily lives: financial, physical, mental, emotional and spiritual. We are currently in Phase 1 of carrying out of the grander vision of “elevating human potential by living a strategically positive life” by offering tools to help with people improve their financial wellness. These are the same tools that have helped me greatly in my quest toward time and money freedom.

Further to that, mounting statistics and researches around the world have shown that “financial wellness” remains a front and centre determinant of one’s quality of life and state of mind. Forget statistics and research results, if we are to take an honest look at ourselves and the people around us, most (if not all) of us can relate to one of these statements or situations:

- The number one factor that breaks up any couple is money. I saw that happen to my parents and many other relationships in my lifetime so far.

- Stresses and worries about money have directly contributed to people’s mental health. I know I was there myself despite making a relatively healthy job income.

- The pressure to maintain and get ahead financially in life has directly caused physical symptoms and illnesses in the modern world.

The list goes on and on. Even a simple Google search on this topic alone was shocking and chilled me to the bone. The positive, though, is that it gave me a much needed dose of confidence and belief of what I stand for these days: increasing the level of financial education to help better people’s financial futures. Truthfully, this has never been about real estate or even real estate investing strategies (shocking, I know). This has always been about leveraging the right investment tool to take care of one very important aspect of our day-to-day lives: money. The most commonly used currency these days that allows us options in life.

I believe that people who are simply looking to buy more real estate aren’t simply the right audience for me or Trust Your Talent. Those who are seeking time and money freedom as a personal vision and a way of living are the ones that will resonate with these messages.

As a result, after bumping around for 4 decades with numerous mentors in my life, I look for those who understand that real estate investing is a means to and end. Those who create financial results through real estate investing to contribute to a bigger vision — in their own lives and into the world. Those who stand for anything less than that…well, they are simply not good enough anymore.

To be completely blunt, there are those who “teach” enough so that I either become their OPM (other people’s money) or have to solely rely on their ‘other paid services’ (ie. legal) in order to completely execute on any deal is a clear red flag. The purpose of offering financial education and elevating a person’s financial intelligence in my LOUD AND OBNOXIOUS opinion should aim at giving them the required tools for independent thinking and decision making when presented with an opportunity (for differentiation between opportunity vs deal, refer back to this article).

THIS quote above (or an ageless wisdom) is always the end goal. That’s why when I seek help these days, it’s to acquire resources, tools, new perspectives and new knowledge to become as good as my Mentor, if not better. I have no problem saying that because I know a few of my students definitely have gone on to doing bigger projects than I have. That is an amazing feeling when the shared vision is not on the size of the deal nor the amount of profit, but the ability to be autonomous and living life on our own terms.

Clearly asking them what their personal vision and mission for offering training and mentoring is a quick and easy way to determined whether you align. There should be ZERO hesitation for true go-giver to explain their purpose and intention being a mentor.

To be continued…

Tomy dedicated readers, I thank you for your support and feedback. If this is the first time you’re reading one of my publications, I hope you’ve enjoyed it and learned a thing or two.

For those of you who prefer watching videos, here is the YouTube channel where some of my work (very raw) has been shared.

And if you’re looking for the quickest way to understand what “financial education through real estate investing” means, we run 1-Day Bootcamps as an introduction. And yes, full disclosure, you’ll have the opportunity to pursue advanced trainings during the Bootcamp if you wish.

(Written at home in Edmonton, AB.)

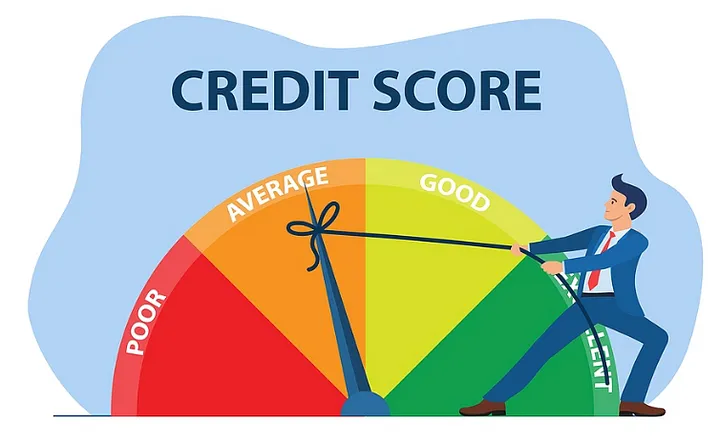

Financial Education: Understanding your Credit Score — the 5 Factors (Part 2/2)

June 21, 2022

Following Part 1, here are the 5 factors that determine our credit score.

Before I get started on this list, I also want to share that this is only ONE PART of credit — meaning: this is only one of the “5 C’s of Credit” you would see loan officers and brokers use to determine whether you would be extended credit when applying. Naturally, that’s coming up in the next article!

Everyday there are people with high credit scores that tend to get very shocked when they are turned down by a mortgage broker, a credit card application or a financial institution. I will continue to put the magnifying glass on credit score here and put the focus on the bigger picture (so to speak) next.

The 5 Factors

- Payment History

First of all, I hope that everyone understands that when you borrow money, it’s your obligation to pay it back to whoever lent it to you unless they specified that it’s a gift that you do not need to pay back. Clearly, even if it’s a small loan between friends and family, chances are they are not going to go to the credit bureau and submit your payment history on you.

So, this largely applies to institutional lending — meaning that licensed lenders who you borrow money from. Even if you’re repaying your debt but are late — either a few times during the time you’re supposed to pay it back, or consistently, this is going to bring your credit score down.

The easiest way to look at this is to turn the table around. How would you rate a friend who borrows money from you and pays it back regularly and in full as agreed VS another friend who you keep on having to chase down to get your money back? Also, are you more likely to lend to someone with a history of bankruptcy or without? Unlike golf, we want high scores here — the higher the better.

2. Amounts Owed

This only matters if you carry an outstanding balance. If you are the type that pays off all your bills on time — especially credit cards, then you’re likely pretty safe here.

This particular factor is also known as ‘utilization rate’. To be honest, you can ask a credit counsellor, a representative from one of the credit bureaus, your banker, a mortgage broker, or even the person who’s sharing all this information with you right now, none of us can provide you with a clear answer on what percentage you should stay under.

Let me take that one step further and this requires some illustration here: some people say to stay below 50% of your credit limit and some say 75% for your credit score to not be impacted negatively. This really only applies to revolving credit accounts — I’ll get to what that means later (in Types of Credit). For now, let’s use a credit card as an example. Also, for demonstration sake, let’s just use 75% as our number here. I would suggest that grab a piece of paper and a pen and write along as you read on.

Say, if your visa account has a credit limit of $10,000 and you’re carrying a balance of $8,000. That is 80% in utilization rate on that account. This will then impact your score negatively and thus bring your score down. 😔 That’s a frown face. I know what some of you want to ask: what if I have a total of $50,000 in credit limit between my 5 credit cards — assuming each card has a credit limit of $10,000, and I only have an outstanding balance of $30,000, which works out to be 60% utilization rate — sounds great, right? Not necessarily! It depends on the breakdown of each card balance. You can very well have 3 cards that are maxed out and 2 cards you pay down regularly (so no outstanding balance), it can and likely will impact your score negatively. So…work with someone (a credit counsellor, a mortgage broker, or a financial wellness Coach — depending on how much help you need) to get this fixed or starting paying some of these down.

3. Length of Credit History

This is probably the most straightforward one of the 5 factors — the longer you’ve had your credit products for (provided that you’ve been a good girl or good boy at paying it back), it can only help your credit score to rise. The logic is that, if you’re delinquent to the point that your lenders refuse you the product, you would not have that account as an active/open account at the time of pulling your credit score and report. Also, if that’s the case, it’ll definitely stay on your credit report not just as an inactive account, but also one that’s involuntarily closed. It’s like a cautionary tale that one lender is sending to your other lenders and, worse yet, all your potential future lenders.

4. New Credit

Some people know this as a ‘pull’ or a ‘hit’ on your credit. The proper term is an ‘inquiry’ — in case you’re wondering. It’s good to know that there are hard inquiries and soft inquiries. One decreases your credit score and one does, well, nothing to it.

If you’ve just ‘inquired about your credit report or credit score’ via one of the websites I suggested, that was a soft inquiry and does NOT impact your credit score negatively. Actually, it doesn’t even matter which site you got it from. The focus is on ‘who’ originated the inquiry. If you’re just checking up on yourself — it’s no different than checking your bank balance or even blood sugar level to make sure you’re on track.

On the other hand, a hard inquiry is like an ex (or soon-to-be ex) looking into your finances, there’s usually an ulterior motive and that’s usually bad.

When do hard inquiries happen, you ask? They happen every time you apply for a credit product —

- a new credit card,

- a line of credit,

- a personal loan,

- a mortgage,

- a car loan,

- a phone plan,

- get your place hooked up with electricity and gas, or

- a retail card to get some furniture or home theatre.

Doing too many of these in a single year can definitely impact your credit score for the worse. How many? Like ‘utilization rate’, I wish I got a solid answer from all industry professionals and even the credit bureaus directly, but no one is making a giant poster with a number on it to show us! However, collectively, our best and deductive conclusion — that’s right, this is more Sherlock Holmes than relying our Spidey sense — is between 4–6 per year. If your score is on the low side to begin with, max it out at 4. If you feel like you have room to stretch, add 2 more times in a year.

Why do hard inquiries decrease your score? The concept is actually quite simple, by definition, hard pulls (just changing it up to get some street cred here…) indicate that you’re actively shopping for a loan of some sort, and you’re making it known. Think of it this way, you ask your Dad for some money, he says yes, then you ask your Mom, she says yes, then you ask your friend, he/she says yes, then you ask your coworker, he/she also says yes. Now you have all this money in your pocket, what’s stopping you from fleeing to sunny Mexico and live like a king or queen, and never return to pay them their money back?

On the other hand, if you’re in need of money and ask your Dad for it, he says no, then you try your Mom, and she says no, you do this for a few more times, by the time you get to person number 7, they are going to wonder why the previous people didn’t lend you any.

Lastly, as a light bulb moment, when it comes to credit, it’s always better to have it and not need it, than to need it and not have it. (This is VERY important.) Repeat this line to yourself LOUDLY (or loudly in your head): WHEN IT COMES TO CREDIT, IT’S ALWAYS BETTER TO HAVE IT AND NOT NEED, THAN TO NEED IT AND NOT HAVE IT.

So, plan your 4–6 hard pulls a year wisely! Just a side note, most credit limit increase requests now require hard pulls as well and now you know what that means!

5. Types of Credit

Finally, we’re talking about the different types of credit. They were briefly mentioned earlier when we were discussing the ‘new credit’ factor.

What exactly are they?

This is probably not the part you need to remember as much as the 5 factors as there are 5 main types that most of us at some point in our lives will inevitably all have — open, revolving, instalments, lines of credit and mortgages.

An open credit type is where the account holder (or the card holder) can draw credit as needed up to a certain amount with the total balance due and payable IN FULL within a specific time frame. Examples would be an American Express charge card, your utilities and cable bills. Basically, an account that you’re not allowed to hold an active balance in it unlike a typical credit card.

Speaking of credit cards, that brings us to the next type that is a “revolving credit”. Think of a revolving door (or maybe even a hamster wheel), a revolving credit is open ended where the cardholder can ‘draw’ credit from the card up to a certain limit, then make regular/required minimum payments. A line of credit often falls under this category as well. A line of credit is usually different from a personal loan in that a line of credit typically requires interest-only payments as long as you continue to pay down your balance. A personal loan often times requires you to make principle-and-interest payments.

That brings us to instalment credit — a personal loan or a car loan usually falls into this category as these loans come with a fixed number of equal payments. If you are still carrying a student loan, chances are, this is where that belongs as well. An instalment loan typically starts with the maximum amount you’re approved to borrow, and, unlike a revolving credit account, that amount can only go down from there.

Lastly, a mortgage. It’s structured similarly to an instalment credit and typically applies only to real estate. Note that a HELOC (home equity line of credit) usually functions more like a regular LOC, thus, more of a revolving credit account.

Conclusion

There you have it! Understanding your credit from an investor’s perspective.

Like everything else, once you understand how it works, it appears simple and you can leverage it to your advantage. When you start learning about the different creative financing strategies and instruments later, you will see how a high credit score is not even a necessity (most of the times).

My Real Conclusion

The credit you carry will be built a lot based on your integrity in the business world. That’s the REAL currency of CREDIT you will also need to pay attention to maintaining.

Tomy dedicated readers, I thank you for your support and feedback. If this is the first time you’re reading one of my publications, I hope you’ve enjoyed it and learned a thing or two.

If you’re wanting to be a part of a community of real estate investors from around the globe, here is the T.A.L.E.N.T.ed Investors Facebook Group. It’s a place where people come together to share experiences, knowledge, successes and challenges, and money making opportunities!

For those of you who prefer watching videos, here is the YouTube channel where some of my work (very raw) has been shared.

Lastly and definitely not least, Bootcamp! If you prefer the live interaction and delivery to help you build some foundation, our next Bootcamp is on July 23 and July 24. Go ahead and register for a session for either day to help you further your financial education.

(Written at home in Edmonton, AB)

3 Lessons that Help me Thrive through Recessions

July 12, 2022

First of all, there are economic vs perceived definitions of what constitutes a recession. After many searches, it’s become weirdly clear to me that everyone agrees on what a recession is:

- “During a recession, the economy struggles, people lose work, companies make fewer sales and the country’s overall economic output declines (Forbes.com).”

- “A recession is a period of declining economic performance across an entire economy that lasts for several months (Investopedia.com).”

- “In economics, a recession is a business cycle contraction when there is a general decline in economic activity (Wikipedia.org).”

Of course, an economic recession can be of any scale — even on a personal level — and it doesn’t necessarily need to be impacting a whole country or even the rest of the world (like the one we seem to be facing at the moment). However, city-wide recessions (such as the City of Detroit in the US) to worldwide recessions (such as the one induced by COVID-19 lockdowns back in the year 2020) still occur once every few decades or even centuries. Remember: everything’s cyclical.

One of the key reasons why I also call it a ‘perceived definition’ is because none of the (what I would call) experts seem to agree with each other on the length of time it takes to clearly define a period of ‘overall economic output decline’ as recession. I don’t know about you, but I personally prefer to look at things this way since I fundamentally believe in not only the possibility of surviving through an economic recession but thriving through one regardless of how long a recession is.

As usual, this article is written largely based on my personal definition and experience, and I’m officially calling what’s happening in the general economic environment a recession (at least, in Canada).

2008

In2008, when global financial crisis was at its peak, I was still only about 18 months into the work force as an economist would call it. Proud of my 6-figure job as a 26 year-old, I thought I was invincible as long as I worked hard and work even harder when I needed to.

Of course, my strategy to trade more hours for dollars didn’t work. More hours, yes. More dollars, no. The shrinking results from my elevated efforts to maintain a pay check and lifestyle forced me to learn some of the “what not to do’s”:

- Cut spending on everything (which I later on learned is actually quite stupid in the grand scheme of things),

- Pay down my mortgage and car loan faster (which I again learned was a financially illiterate move), and

- Put more money into savings and company stock options where they would match 25% on every dollars I put in (which literally makes me angry right now even just writing about it).

What I learned from living through the 2007–2009 global financial crisis set the foundation for how I’ve built everything today.

The real lesson is this:

Spend and invest — but only on necessities and assets especially during an economic downturn. Cost and values have a very direct correlation. Like a bad cell connection on a long-distance call, they are connected but often have lags.

If you don’t know what to invest in, invest in yourself in anyway possible. We are our biggest income generating asset. Many people think investing means that you have to pick a stock, a type of crypto currency these days, some sort of real estate, or (god forbid) savings. That cannot be further from the truth. Nothing will yield good returns if you don’t first decide for yourself if it’s a good investment tool for you. Like all tools, if you don’t know how to use it, it might end up hurting you. I’m pro any type of personal development and financial education (as long as you’re not simply learning how to ‘buy’).

People ask me if real estate is a good investment. I would say: It depends. Are you educated enough to make it a good investment?

People ask me if stocks are a good investment. I would say: It depends. Are you educated enough to make it a good investment?

People ask me if precious metals are a good investment. I would say: It depends. Are you educated enough to make it a good investment?

I think you get the idea. I know for a fact that a newly licensed but trained carpenter can use a hammer more effectively than me.

If you asked me in the beginning of 2010, I would say investing in real estate is horrible!

I became an ‘accidental/traditional’ landlord in 2009 when I moved from my first property. Like many, I rented out the first property because I could afford to carry the ‘expense’ (aka negative cashflow) and the carrying costs of the new one. I also got into a commercial syndication through the referral of a coworker who ‘parked’ her money in real estate in 2009 thinking it would at least do better than my shrinking portfolio in mutual funds, savings and company stock options. Little did I know, I was the last batch of people they took the money from before they gave up on the project. I never saw my hard earned money again.

However, it gave me the kick in the butt that I needed to learn to grow my money and protect my own financial destiny.

Today, I can share with you why I love real estate for days on end as you know. The biggest lesson I took away was this (and still is everyday):

2016

The perfect storm that almost took everything I built.

From 2010–2016…

- Lost all my savings in a commercial real estate syndication

- Began my financial education leveraging real estate investing

- Had my 3rd heart attack and a major depression

- Diagnosed with the 1st of my 5 auto-immune disorders

- Started applying my financial education

- Declared financial freedom (#1) on July 25, 2012 (same day I was laid off from my soul sucking corporate job)

- Declared financial freedom (#2) in December 2015

- In September 2016 — lost $1 million dollars (in cash value) overnight that “almost” lead to a bankruptcy (corporate & personal)

While I thought I was on top of the world at the beginning of 2016, my portfolio was not strong enough to take on the regional recession (in Alberta) that started in 2014. This is why when I teach and mentor these days, it’s not just about cashflow anymore. It’s about cashflow, cashflow management and cashflow mindset. 3 big topics that I plan to write about later.

I’ve learned to indulge and enjoy life the way I want over the years. It can be very unsettling at times when it’s not something you grew up with. For example, I have a 3-hour rule when it comes to flying these days. That means: any flight that is longer than 3 hours, I will pay to fly business or first class. This wasn’t always the case. On smaller planes, I used to walk by the nicer seats and dream that — one day, I would be in it all the time and not have to walk the long way down into “cattle class” (as a British friend of mine puts it). On the bigger planes, I wanted to take the other bridge to board or turn ‘left’ instead of right when entering the aircraft. In the early days, I would upgrade myself with points or ‘get lucky’ and get upgraded because I had some loyalty status with the airlines when some flights were overbooked.

Then, with better financial resources (and mindset), I started with a 6-hour rule. It’s now evolved to the 3-hour rule as I’ve shared. This is not a brag nor a status symbol. Rather, it’s the lesson of taking care of what’s important: health. One of my conditions is called Ankylosing Spondylitis. Feel free to look it up. While I took a huge loss in 2016, I learned to manage and balance my cashflow to maintain a certain lifestyle to honour my top value: Health. More importantly, I learned to be a value-based spender.

People who know me these days know that I have no problem pulling the trigger on a multi-million dollar real estate investment deal when the numbers are good, and yet have a hard time buying a new piece of furniture for the house for a few thousand dollars. Admittedly, a part of me is already ready for the ‘worst’ to happen again and I want to stay alert and be ready.

I once learned that a best and highest-paid boxer would move to a shack 3 months before a major match because he wanted to sharpen his skills and instincts rather than staying in the lap of luxury he’s created for himself from his financial successes. That has spoken to me — deeply.

Everything is cyclical. This recession taught me to be ready for the worst at any time. To capture the moment, to seize the opportunity and to be disciplined and patient daily. My lesson can be summed by with this quote:

2020

AKA the COVID-19 recession.

Recalling what it was like in March 2020 without looking at charts and analysis of what was happening economically, I was both scared and excited. And this little quote came into my head:

Since the beginning of COVID lockdowns…

- Started Trust Your Talent Academy with many of my trusted and educated investors

- Acquired more cashflowing properties in 1 year than the last 5 combined

- Experienced the 2 financially best years in 2020 and 2021 in my life

- Travelled 9 out of the last 18 months (and counting…) when people felt restricted and fearful to do so

Forgive me if you feel that I’m overly excited about the ‘recession’ that we are in or going into. Because I really am. Of course, it sucks to see some people get hurt and it is not about that. It’s about seeing the human spirit during any sort of ‘downturn’ and how we learn and grow from it for the better each time.

Here’s what I realized what I did back in 2008 was utterly and incredibly stupid:

- Cut spending on everything — to get the economy going, spending needs to happen. Money is a currency. Like a current, it needs to flow. When it flows, it connects and revitalizes parts of the economy needed to function and grow. Think of spending like pumping blood into our veins. What happens when that slows down or even stops?

- Pay down my mortgage and car loan faster — “throwing good money after bad” is a good way of looking at this. As inflation rises, your debt obligation shrinks. Read that again. While our money devalues, so does our debt. The point is NOT to pay down debt faster, but to leverage debt even more to acquire income generating assets during times like these.

- Put more money into savings and company stock options where they would match 25% on every dollars I put in — unless you’re the CEO or have insider trading information, I have no other comments other than maybe cash out and tape your money to the back of your toilet at this point. No joke.

Technically, the pattern is simple and can once again be summed up with: everything is cyclical (3rd time’s a charm!).

The financially educated know that there’s another great opportunity coming. I have never personally witnessed 2 economic recessions happen so close to each other. I personally believe that we were headed for a recession right before lockdowns started due to COVID. The global initiative from governments creating aids (aka printing money) coupled with the resulting supply chain issues are making this one seem scarier than it really is.

Not only me, but friends in my circle also experienced some of their best financial results in 2020 from investing in other vehicles — stocks and businesses. The lesson carry through: nothing you choose will create the financial results if you do not first choose to master your own knowledge in it. Moreover, how you DECIDE to come out of this recession will largely determine how you ACTUALLY come out of it.

So, here you have it: my 3 lessons:

- Invest in myself — my financial education, my personal development, my physical health and my mindset

- Honour my values through the good and bad times so I never have to ask “what am I doing it all for?”

- Stay alert and stay humble. Expand my means responsibly.

Gratefully, each ‘recession’ has further helped me define who I am as a person in addition to creating better financial results. I hope it will start to do the same for you.

Tomy dedicated readers, I thank you for your support and feedback. If this is the first time you’re reading one of my publications, I hope you’ve enjoyed it and learned a thing or two.

If you’re wanting to be a part of a community of real estate investors from around the globe, here is the T.A.L.E.N.T.ed Investors Facebook Group. It’s a place where people come together to share experiences, knowledge, successes and challenges, and money making opportunities!

For those of you who prefer watching videos, here is the YouTube channel where some of my work (very raw) has been shared.

If you prefer the live interaction and delivery to help you build some foundation, our next Bootcamp is on July 23 and July 24. Go ahead and register for a session for either day to help you further your financial education.

Lastly, I just want to say thank you for your continuing support.

I aim to be authentic and adding value to your life.

I invest to build a life. I build business to create better life experiences.

It’s ultimately about LIFE and I appreciate you coming on this journey with me!

(Written at the Fairmont Royal York in Downtown Toronto, ON)

Financial Education through Real Estate Investing: Recession & Cashflow Management (Part 1)

July 19, 2022

(WARNING: COLOURFUL LANGUAGE)

Cashflow — another highly used marketing buzz word by real estate buyers who masquerade as investors and coaches to make their ‘deals’ sound better than they are these days. My attempt as usual with this article is this: help as many people understand the difference between cashflow, cashflow management and, MOST IMPORTANTLY, cashflow mindset.

With so many people reaching out these days asking for perspectives, opinions and experiences during a time like this — looming recession and high interest rate (cost of borrowing), I always like to go back to the basics to stay grounded.

According to Investopedia, cashflow is defined as “the movement of money in and out of a company. Cash received signifies inflows, and cash spent signifies outflows. The cash flow statement is a financial statement that reports on a company’s sources and usage of cash over some time.”

First thing first, let’s quickly break this definition down:

- It’s the ‘movement of money’ in and out of a company. If you’ve had the chance to check out some of the My Daily Dose with Tim videos, you’ll know that I treat EACH and EVERY property like an independent business. And like a business, we want to be making a profit at the end of every month (unless it’s meant to be non-profit from the start).

- Cashflow is sometimes synonymous as profit. If you’ve gone to any sort of business school, you’ll learn this very definition in your 101 class: Revenue — Expenses = Profit. As a result, cashflow is also an indicator of how well the business is run — kind of makes sense. At any given point, the goal is to maximize revenue and minimize expenses. That brings me to a very important point here: the emphasis should be on creating POSITIVE CASHFLOW.

- In most real estate investing strategies (refer to the Wheel of Wealth articles), the high level formula actually looks more like this picture (yes, that’s my handwriting on a flip chart — don’t judge 😉):

Well, well, well…it looks like we are missing a crucial component here with the simplified version before: debt service (aka cost of borrowing). Unless you are purchasing your properties with cash (and why would you?!), chances are you need to maintain the debt servicing on a regular basis. And the terms and rates of the debt service will ultimately determine the cashflow/profit.

As I’m writing this, I know many buyers (who have been posing as investors and coaches) have stopped buying while I’m in the process of acquiring/closing on 12 properties (16 doors) from 2 tired landlords — in both Canada and the US. I’m also making the biggest daily gains from trading futures since I started learning last September.

I’m definitely NOT braggin’ since I was not always able to capture every economic downturn to the best of my ability (as mentioned in the previous article). However, I did learn from a mentor at the beginning of my financial education career that Financial education will allow anyone to make money and grow wealth when the market is going up, down and sideways. That was the ‘sales pitch’ that got me. Today, it remains the main reason why I’m pro financial education and NOT just real estate investing.

When you are financially educated, you will learn be excited about economic downturns for these 2 main reasons: