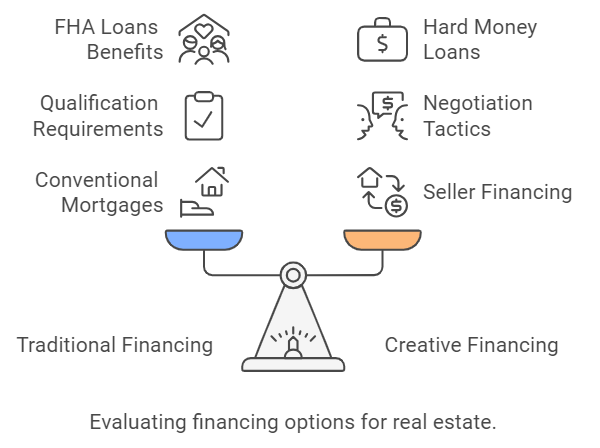

Creative Financing in Real Estate | Unlock Alternative Funding Options

For real estate investors aiming to diversify and grow their portfolios, creative financing strategies offer powerful alternatives to traditional mortgages. By exploring innovative funding methods, investors can access unique opportunities to maximize returns and manage risk. In this guide, we’ll dive into these creative financing options, examine their benefits, and see how they fit into broader real estate investing strategies for a well-rounded investment approach.

Understanding Creative Financing

What is Creative Financing in Real Estate?

Creative financing refers to non-traditional methods of acquiring real estate that often involve unique arrangements between buyers and sellers. These approaches can provide flexibility, reduce costs, and open doors to investment opportunities that might otherwise be inaccessible.

Why Consider Creative Financing?

Advantages of Non-Traditional Methods

Creative financing can be particularly beneficial for investors looking to minimize upfront costs, avoid strict credit checks, or expedite the purchasing process. Here are some key advantages:

Lower Barriers to Entry : Many creative financing methods require less capital upfront, making it easier for new investors to enter the market. “Building and Scaling Your Real Estate Portfolio”

Faster Transactions : By bypassing traditional lenders, investors can often close deals more quickly, seizing opportunities as they arise.

Greater Flexibility: Creative financing arrangements can be tailored to fit both buyer and seller needs, allowing for more innovative deal structures.

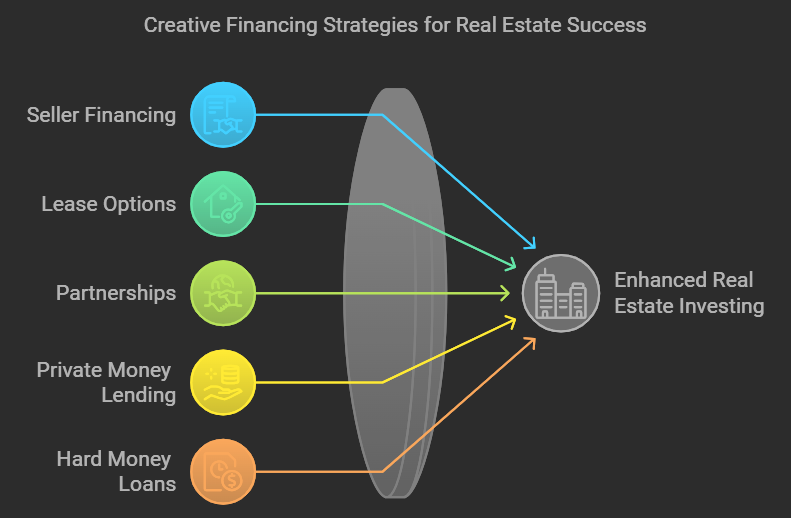

Common Creative Financing Strategies

Here are some popular creative financing techniques that can enhance your real estate investing strategy:

1. Seller Financing

Empowering Buyers Through Direct Deals

In seller financing, the property seller acts as the lender, allowing the buyer to make payments directly to them rather than through a traditional bank. This arrangement can be advantageous for both parties, as it often involves fewer fees and a more straightforward approval process.

2. Lease Options

Rent Now, Buy Later

A lease option empowers investors to rent a property with the flexibility to buy it later. This arrangement allows tenants to build equity while experiencing the property firsthand, giving them confidence before committing to ownership—a choice that complements the decision-making process found in residential vs. commercial real estate investing.

3. Partnerships

Pooling Resources for Greater Success

Forming partnerships can be an effective way to share financial responsibilities and risks. By collaborating with other investors, you can leverage their capital, expertise, and networks to enhance your investment strategy.

4. Private Money Lending

Funding from Individuals

Private money lenders are individuals who provide loans for real estate investments. This funding source can often come with more flexible terms compared to traditional lenders, making it an appealing option for investors seeking quick access to capital.

5. Hard Money Loans

Short-Term Solutions for Quick Deals

Hard money loans, secured by real estate, are offered by private investors or firms. While they come with higher interest rates and shorter terms, they provide quick funding for investors pursuing immediate property flips or other time-sensitive acquisitions. Understanding the potential risks tied to this type of financing is essential—especially as part of a broader approach to “risk management and insurance in real estate investing”.

Implementing Creative Financing Strategies

Tips for Successful Execution

To successfully implement creative financing strategies, consider the following steps:

- Research Your Options

Familiarize yourself with different creative financing methods to determine which aligns best with your investment goals. - Network with Other Investors

Building relationships with experienced investors can provide insights and opportunities for partnerships or alternative financing arrangements. - Consult Professionals

Working with real estate agents, attorneys, and financial advisors who understand creative financing can help you navigate the complexities of these strategies.

Conclusion

Creative financing offers real estate investors innovative ways to expand portfolios and boost profitability. By exploring options such as seller financing, lease options, and private lending, you can unlock strategies that align with your financial goals. For more insights on real estate investing strategies , take advantage of Trust Your Talent Academy’s free webinars and upcoming events. Here, we provide expert mentorship and practical resources designed to set you on a successful real estate journey.

Begin your path to financial independence with creative financing methods that work for you, and take your next step toward building “sustainable wealth through real estate” _ Real Estate for Financial Independence: Creating Sustainable Wealth’.

FAQs

Creative financing encompasses innovative funding methods for real estate investments that extend beyond traditional mortgage options. Strategies like seller financing, lease options, and hard money loans are all examples that can help investors expand their portfolios.

In seller financing, the property seller serves as the lender, allowing the buyer to make payments directly to them instead of going through a bank. This can facilitate a quicker sale and offer flexible terms for buyers who may have difficulty securing traditional financing.

A lease option allows tenants to rent a property with the potential to purchase it later. This strategy gives them the chance to build equity while assessing whether the property meets their needs before making a commitment.

Hard money loans are short-term loans secured by real estate, typically provided by private investors or companies. Although they often come with higher interest rates, these loans can be advantageous for investors needing immediate financing for urgent purchases or property flips.

Using creative financing can lead to greater flexibility, faster access to capital, and the ability to acquire properties that might not qualify for traditional financing. This approach can also assist investors in mitigating risks and maximizing their overall profitability.

Absolutely! Beginners can successfully use creative financing strategies by educating themselves about their options and seeking guidance. Resources like free webinars and mentorship programs provide valuable insights and support for new investors.

To dive deeper into real estate investing strategies, explore educational resources offered by Trust Your Talent Academy. They provide a variety of materials, including upcoming events and free webinars designed to equip you with the knowledge needed to succeed in your investment journey.

Rental Property Management: From Tenant Screening to Passive Income

Managing a rental property can be highly rewarding, offering a steady income stream and long-term wealth building. However, effective property management requires a well-planned strategy to reduce risks and maximize returns. In this guide, we’ll take you through the essential steps of rental property management, from tenant screening to generating passive income.

Understanding the Basics of Rental Property Management

What is Rental Property Management?

Rental property management involves overseeing the daily operations of a real estate rental property. This includes everything from finding tenants and handling maintenance requests to collecting rent and ensuring legal compliance. To deepen your understanding of how rental properties fit into the broader picture of real estate investing, explore our Real Estate Investing Strategies guide.

Why Effective Management Matters

Efficient property management can mean the difference between a highly profitable investment and one that loses money. Proper management helps maintain tenant satisfaction, preserve property value, and ensure consistent rental income. “Building and Scaling Your Real Estate Portfolio”.

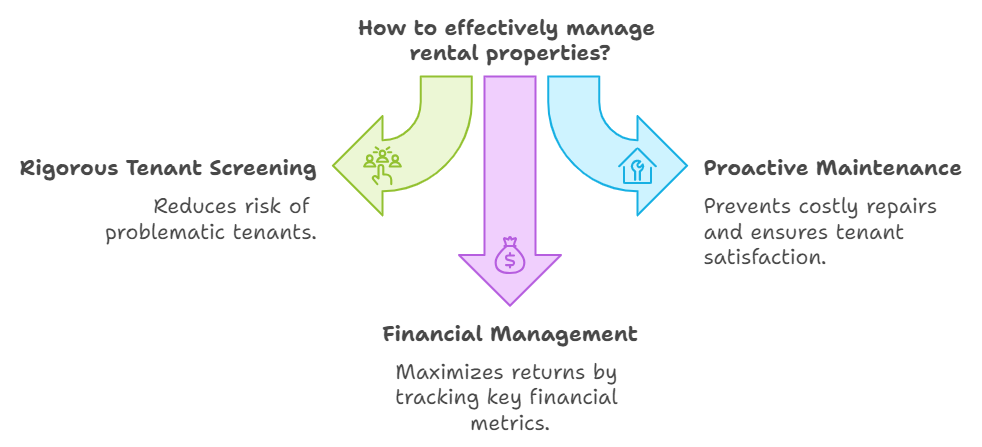

Tenant Screening: The Foundation of a Profitable Rental

Why Tenant Screening is Critical

Selecting the right tenant is one of the most important aspects of property management. Good tenants pay on time, take care of the property, and minimize potential problems. To learn more about how tenant selection can impact your investment strategy, check out our insights on Fix and Flip vs. Buy and Hold: Comparing Popular Investment Strategies.

Steps to Screen Tenants Effectively

- Credit Checks: Review credit history to ensure tenants can manage financial obligations.

- Background Checks: Check for criminal records and eviction history to identify potential risks.

- Income Verification: Ensure that the tenant’s income is sufficient to cover rent and other living expenses.

- References: Speak to previous landlords to assess the tenant’s rental history.

Property Maintenance: Keeping Your Investment in Good Condition

Preventative vs. Reactive Maintenance

Preventative maintenance is crucial to avoiding costly repairs and maintaining the property’s value. Reactive maintenance involves fixing issues as they arise, but a proactive approach is always better. “Risk Management and Insurance in Real Estate Investing”

Common Maintenance Tasks

- Regular HVAC inspections

- Roof and plumbing checks

- Landscaping and exterior upkeep

- Seasonal maintenance (snow removal, gutter cleaning)

Hiring a Property Manager vs. DIY Maintenance

While some landlords handle maintenance themselves, hiring a professional property manager can save time and reduce stress, especially for larger portfolios. Understanding the implications of property management can be crucial, particularly when considering different investment types. Explore more in our article on Residential vs. Commercial Real Estate Investing: Choosing Your Path.

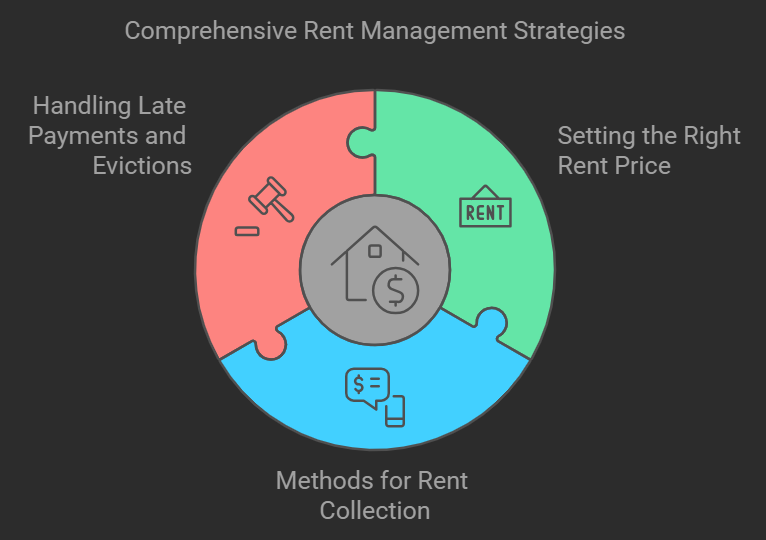

Rent Collection and Financial Management

Setting the Right Rent Price

Methods for Rent Collection

- Online Payment Platforms: Convenient and secure for both landlords and tenants.

- Traditional Payment Methods: Checks or cash, though less common today.

Handling Late Payments and Evictions

Late payments can disrupt your cash flow, so it’s important to have clear policies in place. If a tenant consistently fails to pay, you may need to consider legal eviction proceedings.

Explore our guide on Efficient Rent Collection Strategies to avoid common pitfalls.

“Efficient Rent Collection Strategies”

Legal Compliance and Tenant Rights

Understanding Landlord-Tenant Laws

Each region has specific laws governing rental agreements, tenant rights, and eviction procedures. Ensuring compliance can protect you from legal disputes.

Key Documents Every Landlord Should Have

- Lease Agreement

- Move-In/Move-Out Inspection Forms

- Tenant Notices (late payments, eviction notices, etc.)

Learn more about staying compliant in our Legal Compliance Guide for Rental Property Owners.

“Legal Compliance Guide for Rental Property Owners”

Maximizing Passive Income: Turning Your Rental into a Profitable Business

What is Passive Income in Real Estate?

Passive income refers to earnings generated with minimal active involvement. In rental property management, this can be achieved by automating tasks and delegating responsibilities. “Real Estate for Financial Independence: Creating Sustainable Wealth”

Strategies to Maximize Passive Income

- Hire a Property Management Company: Delegate day-to-day tasks while collecting passive rental income.

- Invest in Technology: Use property management software to streamline tenant communications, rent collection, and maintenance requests.

- Expand Your Portfolio: As you acquire more rental properties, your potential for passive income increases, especially if managed efficiently.

Conclusion: From Active Management to True Passive Income

Managing a rental property is a balancing act between hands-on involvement and automated systems. By effectively screening tenants, maintaining the property, staying compliant with laws, and automating processes, you can reduce stress and maximize returns, ultimately turning your rental property into a source of steady passive income. This journey begins with understanding essential real estate investing strategies to ensure your success.

To further enhance your skills in property management and real estate investing, consider the resources offered by Trust Your Talent Academy. We’re committed to providing you with the knowledge and tools needed to thrive in the dynamic world of real estate.

Ready to take your real estate investing skills to the next level? Explore our comprehensive courses tailored to investors at all stages, from beginners to seasoned professionals. For personalized guidance, consider scheduling a strategy session with one of our expert mentors. And don’t miss our upcoming events, where you can network with fellow investors and learn from industry leaders.

FAQs: Rental Property Management

A combination of credit checks, background checks, income verification, and reference checks ensures you find reliable tenants.

Online payment platforms like PayPal or dedicated property management software can simplify rent collection and reduce late payments.

If you own multiple properties or prefer a hands-off approach, hiring a property manager can help you focus on passive income generation while ensuring your properties are well-managed.

Regular property maintenance, strategic rent pricing, and investing in technology can increase tenant satisfaction, reduce vacancies, and improve income potential.

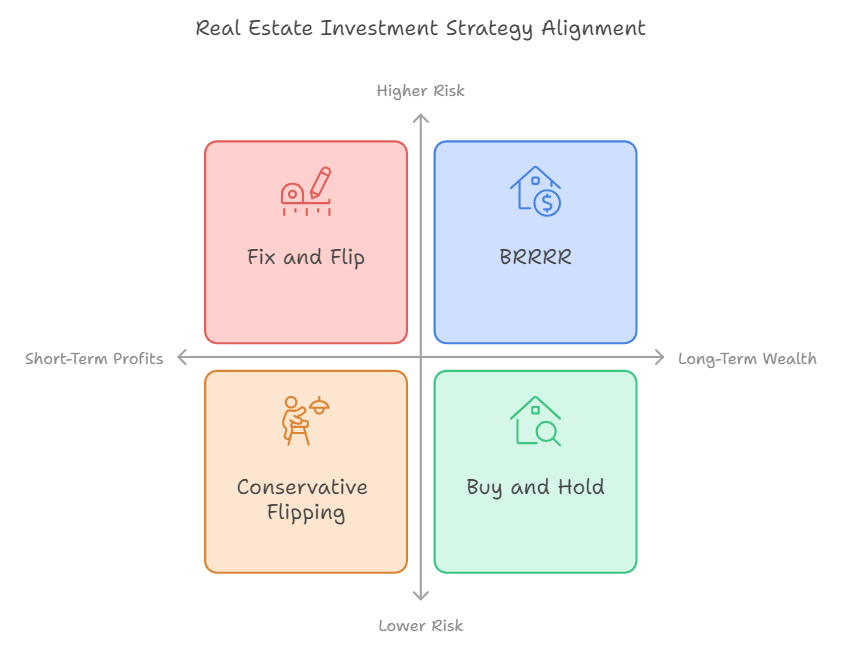

Fix and Flip vs. Buy and Hold: Comparing Popular Investment Strategies

In the world of real estate investing, two strategies often stand out: Fix and Flip, and Buy and Hold. Each approach offers unique advantages and challenges, catering to different investor goals and market conditions. This guide will help you understand both strategies in depth, allowing you to make an informed decision on which path aligns best with your investment objectives.

For a broader overview of real estate investing strategies, check out our comprehensive guide on Real Estate Investing Strategies.

Fix and Flip Strategy

What is Fix and Flip?

Fix and Flip involves purchasing a property, renovating it to increase its value, and then selling it for a profit, typically within a short timeframe.

Key Characteristics of Fix and Flip

- Short-term investment: Usually completed within 3-12 months

- Active involvement: Requires hands-on management of renovations

- Potential for quick profits: Can yield significant returns in a short period

- Higher risk: Market fluctuations and unexpected renovation costs can impact profitability

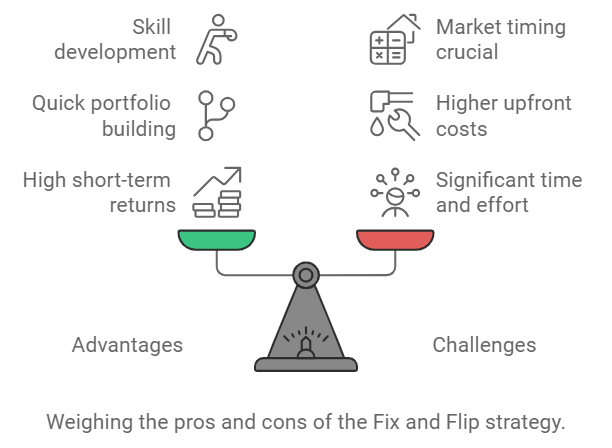

Advantages of Fix and Flip

- Potential for high short-term returns

- Opportunity to build a portfolio quickly

- Develop valuable skills in property valuation and renovation

Challenges of Fix and Flip

- Requires significant time and effort

- Higher upfront costs for renovations

- Market timing is crucial for maximizing profits

- Potential for unexpected expenses during renovation

Learn more about renovation strategies and cost management in our guide to property renovation.

Buy and Hold Strategy

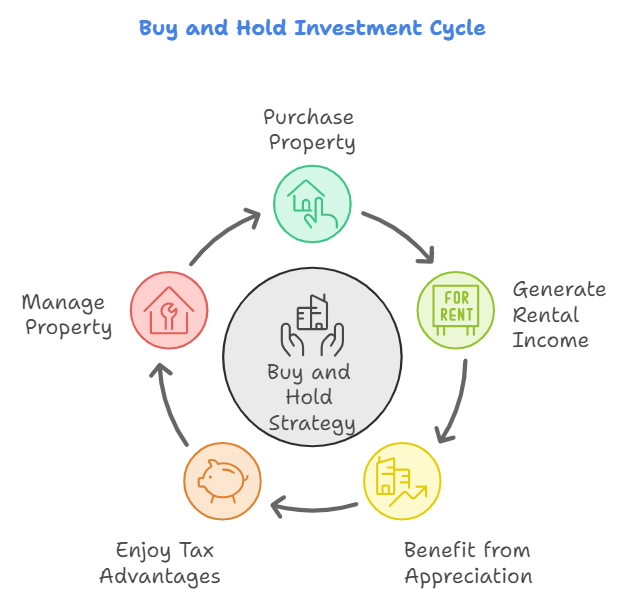

What is Buy and Hold?

Buy and Hold involves purchasing a property with the intention of holding onto it for an extended period, typically generating income through rentals and benefiting from long-term appreciation.

Key Characteristics of Buy and Hold

- Long-term investment: Often held for 5+ years

- Passive income potential: Regular rental income

- Appreciation benefits: Profit from property value increases over time

- Tax advantages: Potential for deductions on mortgage interest and property depreciation

Advantages of Buy and Hold

- Steady, passive income stream

- Long-term appreciation potential

- Tax benefits for rental property owners

- Build equity as tenants pay down the mortgage

Challenges of Buy and Hold

- Requires ongoing property management

- Potential for problem tenants

- Market downturns can impact property values

- Less liquid investment compared to stocks or bonds

Discover effective tenant management strategies in our rental property management guide.

Comparing the Strategies

Financial Considerations

Fix and Flip

- Higher upfront costs for renovations

- Potential for quicker returns

- Short-term capital gains tax implications

Buy and Hold

- Lower ongoing costs (after initial purchase)

- Steady, long-term income potential

- Long-term capital gains tax benefits

For a detailed comparison of tax implications, see our guide on tax strategies for real estate investors.

Time and Effort

Fix and Flip

- Intensive short-term involvement

- Requires active management of renovations and sales process

Buy and Hold

- Less intensive day-to-day involvement

- Requires ongoing property management (can be outsourced)

Market Timing

Fix and Flip

- Highly dependent on market conditions for profitable sales

- Requires accurate prediction of short-term market trends

Buy and Hold

- Less affected by short-term market fluctuations

- Benefits from long-term market appreciation

Learn more about market analysis techniques in our real estate market analysis guide.

Skill Set Required

Fix and Flip

- Renovation and project management skills

- Market analysis for quick turnaround

- Negotiation skills for purchases and sales

Buy and Hold

- Property management skills (or ability to hire managers)

- Tenant screening and relations

- Long-term market analysis

Choosing the Right Strategy for You

Factors to Consider

- Financial goals: Short-term profits vs. long-term wealth building

- Time availability: Active vs. passive involvement

- Risk tolerance: Higher short-term risk vs. lower long-term risk

- Market conditions: Hot sellers’ market vs. stable rental market

- Personal skills and interests: Renovation expertise vs. property management

Hybrid Approaches

Some investors combine elements of both strategies:

- BRRRR (Buy, Rehab, Rent, Refinance, Repeat)

- Fix, flip, and hold a portion of properties

Learn more about creative real estate investing strategies in our comprehensive guide.

Tools and Resources

For Fix and Flip Investors

- Renovation cost estimators

- Local market analysis tools

- Contractor management software

For Buy and Hold Investors

- Property management platforms

- Tenant screening services

- Long-term real estate market forecasting tools

Explore more real estate investing tools and technologies in our guide to leveraging technology in real estate investing.

Conclusion

Both Fix and Flip and Buy and Hold strategies offer unique paths to real estate investing success. Your choice should align with your financial goals, risk tolerance, and personal strengths. Remember, many successful real estate investors incorporate elements of both strategies as they build their portfolios.

At Trust Your Talent Academy, we believe that education is the foundation of successful real estate investing. Whether you’re leaning towards fix and flip or buy and hold, our comprehensive courses can provide you with the knowledge and skills you need to excel in your chosen strategy.

Ready to take the next step in your real estate investing journey? Here are some ways to leverage our resources:

- Schedule a strategy session with one of our expert mentors to develop a personalized investment plan tailored to your goals and resources.

- Explore our course catalog to find specialized training in fix and flip techniques, buy and hold strategies, and everything in between.

- Connect with like-minded investors and industry experts at our upcoming events, including workshops, seminars, and networking opportunities.

Remember, successful real estate investing is not just about choosing the right strategy—it’s about continuous learning, adaptation, and growth. Trust Your Talent Academy is here to support you every step of the way on your path to financial independence through real estate investing.

Frequently Asked Questions

Both can be suitable for beginners, depending on their skills and resources. Buy and hold might be less intensive to start, while fix and flip can provide valuable hands-on experience.

The initial investment varies greatly depending on your location and the type of properties you’re targeting. Generally, fix and flip requires more upfront capital for renovations.

Yes, many investors pursue fix and flip as a full-time career. However, it requires significant time, effort, and expertise to be consistently successful.

Fix and flip profits are typically taxed as ordinary income, while buy and hold can offer tax advantages through depreciation and long-term capital gains.

Residential vs. Commercial Real Estate Investing: Choosing Your Path

When venturing into real estate investing, one of the first crucial decisions you’ll face is choosing between residential and commercial properties. Each path offers unique opportunities and challenges, catering to different investor goals and risk tolerances. In this guide, we’ll explore the key differences, pros, and cons of residential and commercial real estate investing to help you make an informed decision.

Understanding Residential Real Estate Investing

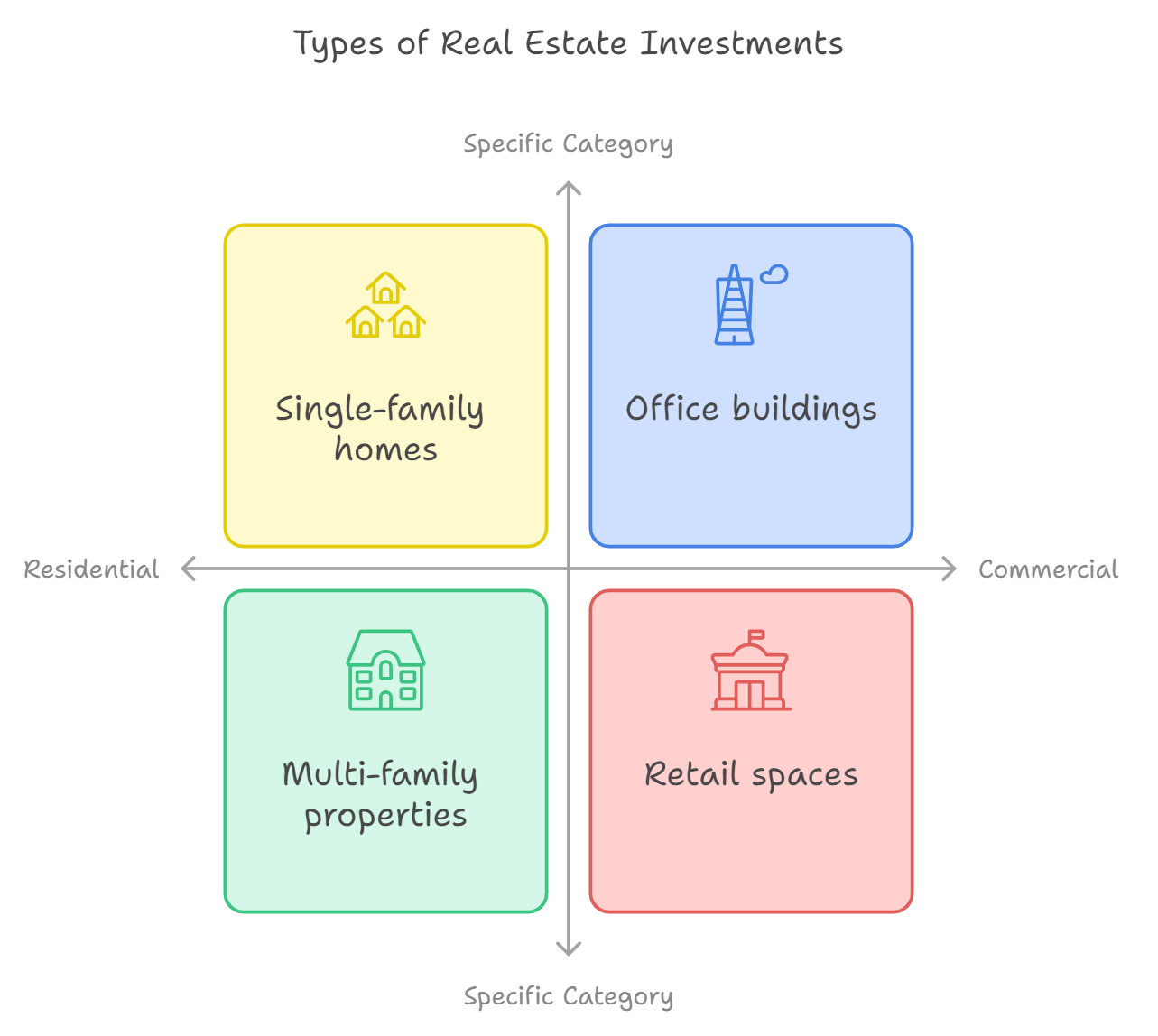

Types of Residential Properties

- Single-family homes

- Multi-family properties (duplexes, triplexes, apartment buildings)

- Condominiums and townhouses

Advantages of Residential Investing

- Lower barrier to entry

- Easier to understand and manage

- More stable market demand

- Potential for house hacking (living in one unit while renting others)

Challenges in Residential Investing

- Potentially lower returns compared to commercial properties

- More hands-on management required

- Impact of personal-use laws and regulations

For more insights on managing residential properties, check out our guide on Rental Property Management: From Tenant Screening to Passive Income.

Exploring Commercial Real Estate Investing

Types of Commercial Properties

- Office buildings

- Retail spaces

- Industrial properties

- Multi-use buildings

- Hotels and hospitality properties

Advantages of Commercial Investing

- Potential for higher returns

- Longer lease terms

- Triple net leases (tenants cover property expenses)

- Opportunity for larger-scale investments

Challenges in Commercial Investing

- Higher initial capital requirements

- More complex management and operations

- Greater susceptibility to economic fluctuations

- Longer vacancy periods between tenants

Learn more about scaling your investments in our article on “Building and Scaling Your Real Estate Portfolio”.

Comparing Financial Aspects

Return on Investment (ROI)

- Residential: Typically 1-4% annual cash-on-cash return

- Commercial: Potentially 6-12% annual cash-on-cash return

Financing Options

- Residential: More straightforward, often with lower interest rates

- Commercial: More complex, usually requiring larger down payments

For a deep dive into financing strategies, explore our guide on Creative Financing in Real Estate: Beyond Traditional Mortgages.

Risk Assessment

Market Volatility

- Residential: Generally more stable, tied to housing needs

- Commercial: More volatile, closely tied to economic cycles

Tenant Considerations

- Residential: Higher turnover, but easier to find new tenants

- Commercial: Lower turnover, but potentially longer vacancies

Legal and Regulatory Considerations

Zoning Laws

- Residential: Typically simpler zoning requirements

- Commercial: More complex zoning and use restrictions

Lease Agreements

- Residential: Standardized, shorter-term leases

- Commercial: Customized, longer-term leases with more negotiation

For more on legal structures in real estate investing, refer to our article on Tax Strategies and Legal Structures for Real Estate Investors.

Technology Impact

Property Management Tools

- Residential: Many user-friendly options available

- Commercial: More specialized, feature-rich software required

Virtual Tours and Marketing

- Residential: Becoming standard practice

- Commercial: Essential for attracting tenants, especially in office and retail spaces

Discover more about leveraging technology in real estate in our guide on Technology in Real Estate: Leveraging AI, VR, and Analytics Tools.

Making Your Decision

Consider these factors when choosing between residential and commercial real estate investing:

- Your investment goals and risk tolerance

- Available capital and financing options

- Time commitment and management preferences

- Local market conditions and opportunities

- Your knowledge and experience in real estate

Remember, many successful investors incorporate both residential and commercial properties in their portfolios to diversify their investments and balance risk and returns.

Conclusion

Both residential and commercial real estate investing offer viable paths to building wealth and achieving financial independence. Your choice should align with your personal goals, resources, and risk tolerance. Whichever path you choose, continuous education and staying informed about market trends are key to success.

Ready to dive deeper into real estate investing strategies? Explore our comprehensive Real Estate Investing Strategies Guide for more insights and expert advice.

FAQ

Residential real estate focuses on housing individuals, such as single-family homes, duplexes, or apartments, while commercial real estate includes offices, retail spaces, and industrial properties. Residential properties cater to stable housing demand, while commercial investments offer higher returns but are more influenced by economic cycles.

Commercial properties often have higher potential returns, ranging from 6-12% cash-on-cash annually, compared to residential returns, which typically range from 1-4%. However, commercial investments come with higher risks and management complexities.

Easier to understand and manage, especially for beginner investors

Lower initial capital requirements

Stable demand due to consistent housing needs

Opportunity for “house hacking” by living in one unit and renting out others

Higher potential returns over time

Longer lease terms provide steady cash flow

Triple net leases transfer property expenses to tenants

Opportunities for scaling investments through larger deals

Residential real estate loans are typically easier to secure with lower interest rates and smaller down payments. Commercial real estate loans are more complex, often requiring larger down payments and detailed financial analysis from lenders.

Commercial properties are more vulnerable to economic downturns, leading to longer vacancy periods and fluctuations in property values. They also require higher initial investments and more complex management.

Yes, residential properties are generally easier to manage, especially with the availability of tenant management tools. Commercial properties demand more expertise and specialized software to handle leases, maintenance, and tenant relations.

Yes, many successful investors diversify their portfolios by investing in both residential and commercial properties. This strategy helps balance risk and returns by leveraging the stability of residential markets with the higher returns of commercial investments.

Residential: Simple lease structures and zoning laws, with regulations that protect tenants

Commercial: More complex lease agreements, customized negotiations, and stricter zoning requirements

Residential properties tend to provide more stable returns as housing demand remains consistent. Commercial properties can offer higher returns, but they are more affected by economic cycles and tenant turnover.

House hacking is a strategy where investors live in one part of a multi-family property while renting out other units to generate rental income. This method reduces living expenses and helps build equity over time.

Residential: User-friendly property management apps and virtual tour platforms

Commercial: Advanced property management software for leases and tenant tracking, along with virtual reality tools to attract tenants

Commercial real estate is more susceptible to economic downturns and market volatility. Residential properties, being tied to essential housing needs, tend to remain more stable during economic shifts.

Your investment goals and risk tolerance

Available capital and financing options

Time commitment for management

Local market conditions and opportunities

Your experience and knowledge of the real estate sector

Real Estate Investing Strategies: Your Comprehensive Guide to Building Wealth

Real estate investing stands as one of the most reliable paths to building long-term wealth and achieving financial independence. This comprehensive guide will walk you through the essential strategies, concepts, and considerations you need to succeed in the world of real estate investing.

Why Invest in Real Estate?

Real estate offers several unique advantages as an investment vehicle:

- Potential for steady cash flow through rental income

- Long-term appreciation of property values

- Tax benefits and deductions

- Leverage to build wealth using other people’s money (OPM)

- Hedge against inflation

Types of Real Estate Investments

Real estate investments come in various forms, each with its own set of advantages and challenges:

Residential Real Estate

- Single-family homes

- Multi-family properties (duplexes, triplexes, apartment buildings)

- Condominiums and townhouses

Commercial Real Estate

- Office buildings

- Retail spaces

- Industrial properties

- Multi-use buildings

For an in-depth comparison of these options, explore our guide on Residential vs. Commercial Real Estate Investing: Choosing Your Path.

Popular Real Estate Investing Strategies

Buy and Hold Strategy

The buy and hold strategy involves purchasing properties with the intention of holding them for an extended period. This approach can provide both ongoing rental income and long-term appreciation.

Key Considerations for Buy and Hold

- Location selection

- Property management

- Financing options

- Tax implications

Fix and Flip Strategy

Fix and flip involves purchasing undervalued properties, renovating them, and selling them for a profit. This strategy requires a keen eye for potential and strong project management skills.

Steps in a Successful Fix and Flip

- Finding undervalued properties

- Accurately estimating renovation costs

- Managing the renovation process

- Marketing and selling the property

To understand which strategy might be best for your goals and risk tolerance, check out our detailed comparison: Fix and Flip vs. Buy and Hold: Comparing Popular Investment Strategies.

Mastering Rental Property Management

Effective property management is crucial for maximizing returns on your real estate investments.

Tenant Screening and Selection

Key Aspects of Tenant Screening

- Credit checks

- Employment verification

- Rental history

- Criminal background checks

Maintenance and Repairs

Proactive Maintenance Strategies

- Regular property inspections

- Preventive maintenance schedules

- Building a reliable contractor network

Financial Management of Rental Properties

Essential Financial Metrics to Track

- Net Operating Income (NOI)

- Cap Rate

- Cash-on-Cash Return

- Return on Investment (ROI)

Learn more about maximizing your rental property potential in our guide: Rental Property Management: From Tenant Screening to Passive Income.

Financing Your Real Estate Ventures

Understanding various financing options is crucial for real estate investors.

Traditional Financing Methods

Conventional Mortgages

- Pros and cons

- Qualification requirements

FHA Loans

- Benefits for owner-occupants

- Limitations for investors

Creative Financing Strategies

Seller Financing

- How it works

- Negotiation tactics

Hard Money Loans

- When to use the

- Calculating costs and risks

Explore alternative financing strategies in our comprehensive article: Creative Financing in Real Estate: Beyond Traditional Mortgages.

Data-Driven Decision Making in Real Estate

Leveraging data and analytics can give you a significant edge in today’s competitive market.

Market Analysis Techniques

Comparative Market Analysis (CMA)

- Steps to conduct a CMA

- Interpreting CMA results

Demographic Trend Analysis

- Key demographic indicators to watch

- How demographic shifts impact real estate markets

Predictive Analytics in Real Estate

Machine Learning Models

- How AI predicts property values

- Using predictive models in your investment strategy

Dive deeper into market analysis techniques with our expert guide: Real Estate Market Analysis: Data-Driven Decision Making for Investors.

Building and Scaling Your Real Estate Portfolio

As you gain experience and capital, you’ll want to expand your real estate portfolio strategically.

Diversification Strategies

Geographic Diversification

- Pros and cons of investing in multiple markets

- How to research new markets effectively

Property Type Diversification

- Balancing residential and commercial investments

- Exploring niche property types (e.g., student housing, senior living)

Scaling Challenges and Solutions

Property Management at Scale

- When to hire a property management company

- Building systems for efficient portfolio management

Financing Growth

- Leveraging equity in existing properties

- Exploring commercial lending options

Learn how to take your investments to the next level with our insights on [Building and Scaling Your Real Estate Portfolio].

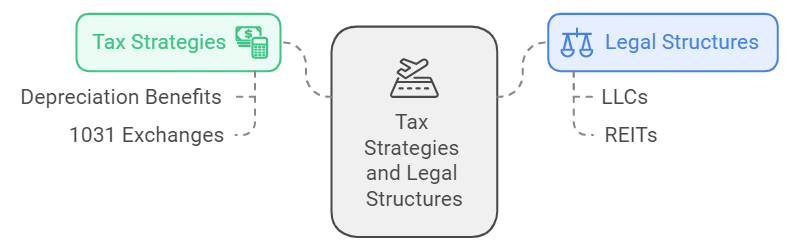

Navigating Tax Strategies and Legal Structures

Optimizing your tax strategy and choosing the right legal structure can significantly impact your bottom line.

Tax Strategies for Real Estate Investors

Depreciation Benefits

- Understanding straight-line vs. accelerated depreciation

- Bonus depreciation opportunities

1031 Exchanges

- Rules and requirements

- Strategic use in portfolio growth

Legal Structures for Real Estate Investing

Limited Liability Companies (LLCs)

- Benefits of using LLCs for real estate

- Single-member vs. multi-member LLCs

Real Estate Investment Trusts (REITs)

- How REITs work

- Pros and cons for investors

Get expert advice on maximizing your returns and protecting your assets in our guide: [Tax Strategies and Legal Structures for Real Estate Investors].

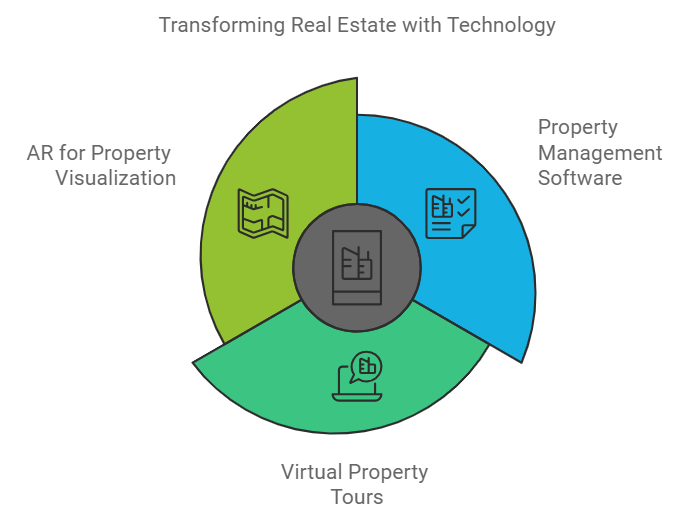

Leveraging Technology in Real Estate Investing

The real estate industry is being transformed by technology.

Property Management Software

Features to Look For

- Rent collection and financial tracking

- Maintenance request management

- Tenant communication tools

Virtual and Augmented Reality in Real Estate

Virtual Property Tours

- Benefits for investors and tenants

- Tools for creating virtual tours

AR for Property Visualization

- Using AR for renovation planning

- AR in commercial property marketing

Discover how to harness the power of technology in your investing journey: [Technology in Real Estate: Leveraging AI, VR, and Analytics Tools].

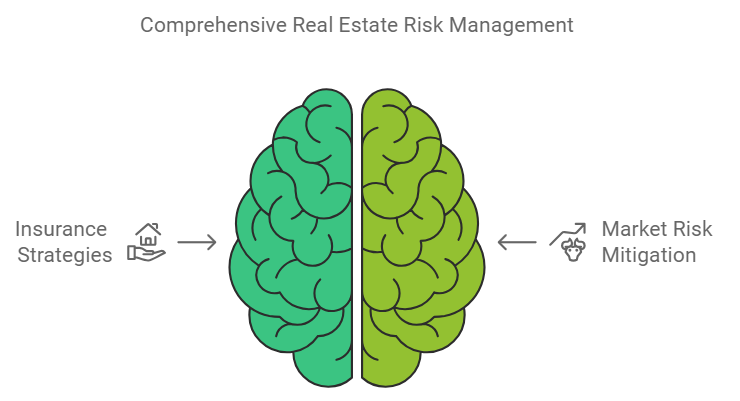

Managing Risk in Real Estate Investments

While real estate can be lucrative, it’s important to understand and mitigate potential risks.

Insurance Strategies

Property Insurance Essentials

- Coverage types for different property classes

- Determining appropriate coverage levels

Liability Protection

- Umbrella policies for real estate investors

- The role of LLCs in liability protection

Market Risk Mitigation

Diversification Tactics

- Balancing your portfolio across markets and property types

- Using REITs for additional diversification

Exit Strategies

- Planning for market downturns

- When and how to sell properties strategically

Learn more about safeguarding your real estate portfolio in our comprehensive guide: [Risk Management and Insurance in Real Estate Investing].

Achieving Financial Independence Through Real Estate

Real estate investing can be a powerful tool for achieving financial independence.

Building Passive Income Streams

Rental Property Strategies

- Maximizing cash flow from rentals

- Strategies for reducing vacancies

Note Investing

- How to invest in real estate notes

- Pros and cons of note investing

Wealth Accumulation Through Appreciation

Long-term Hold Strategies

- Identifying properties with high appreciation potential

- Balancing cash flow and appreciation

Forced Appreciation Techniques

- Value-add strategies for commercial properties

- Renovation tactics for residential investments

Discover strategies for creating sustainable wealth through real estate in our article: [Real Estate for Financial Independence: Creating Sustainable Wealth].

Conclusion: Your Next Steps in Real Estate Investing

Embarking on your real estate investing journey requires education, strategy, and ongoing learning. At Trust Your Talent Academy, we’re committed to providing you with the knowledge and tools needed to succeed in the dynamic world of real estate investing.

Ready to take your real estate investing skills to the next level? Explore our comprehensive courses tailored to investors at all stages. For personalized guidance, consider scheduling a strategy session with one of our expert mentors. And don’t miss our upcoming events, where you can network with fellow investors and learn from industry leaders.

Remember, successful real estate investing is a journey, not a destination. With the right education, strategies, and mindset, you’re well on your way to building lasting wealth through real estate.

Frequently Asked Questions

The amount needed varies depending on the investment strategy and market. Some options, like house hacking or wholesaling, can be started with minimal capital. Traditional property purchases typically require a down payment of 20-25% of the property value.

Like any investment, real estate comes with risks. However, with proper education, due diligence, and risk management strategies, many of these risks can be mitigated. Diversification and thorough market research are key to reducing risk.

Good deals can be found through various channels, including:

Multiple Listing Service (MLS)

Off-market properties (direct mail, networking)

Foreclosures and auctions

Real estate wholesalers

Developing a strong network and using data-driven analysis can help identify promising opportunities.

Both approaches have merits. Investing locally allows for easier property management and better market knowledge. However, investing in other markets can provide diversification and potentially better returns. The decision should be based on your investment goals, risk tolerance, and market conditions.

Key factors to consider include:

Location and neighborhood trends

Property condition and potential renovation costs

Rental income potential

Appreciation prospects

Local economic indicators

Utilize tools like comparative market analysis and cash flow calculations to assess potential investments.

Best Ways to Save for Retirement in Canada: Trust Your Talent

Planning for retirement can feel overwhelming, but it doesn’t have to be! Think of it as a journey where you’re in the driver’s seat, steering towards a secure financial future. In Canada, there are so many smart strategies to help you save for retirement, ensuring you can enjoy those well-deserved golden years without a financial worry. So, let’s dive into the best ways to save for retirement in Canada and tackle some of the common questions you might have along the way.

What Are the Best Ways to Save for Retirement in Canada?

- Start Early: Here’s the secret: the sooner you start saving, the better! By beginning in your 20s, you’ll harness the magic of compound interest. Just imagine your money working for you over the years while you focus on living your life.

- Utilize Registered Accounts: Don’t overlook the power of registered accounts like the Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA). These accounts are designed to give you a boost with tax benefits that can make a big difference in your savings.

- Diversify Investments: Think of diversifying your investments like creating a balanced meal. You want a mix of stocks, bonds, and mutual funds to keep things healthy and minimize risk. This way, you can optimize your growth while protecting your investments from the unpredictable market.

- Employer Contributions: If your job offers a pension plan or matches your retirement savings, make sure to take full advantage of it! This is essentially free money that can significantly grow your retirement funds without you having to lift a finger.

- Set Realistic Goals: Establish clear, achievable savings goals. Knowing exactly how much you need to save can motivate you to stay focused. For more assistance with goal-setting, check out our guide on how much money do you need to retire in Canada—it’s packed with useful insights.

How Much Should You Save for Retirement?

Determining how much you should save depends on your lifestyle, expenses, and income sources. A good rule of thumb is to aim for a retirement income that’s 70% to 80% of what you’re earning now. So, if you’re making $75,000 a year, plan for about $52,500 to $60,000 per year in retirement. It’s all about keeping your lifestyle comfortable!

What Investment Strategies Work Best for Retirement?

Effective investment strategies are like the roadmap to your retirement savings. Here are a few methods to consider:

- Target-Date Funds: These funds automatically adjust their asset allocation as you near retirement age, allowing you to sit back and relax while your investments take care of themselves.

- Robo-Advisors: Want a hassle-free investment experience? Robo-advisors can create a personalized portfolio based on your risk tolerance and goals, simplifying the investment process for you.

- Real Estate Investments: Investing in rental properties can provide you with a steady income stream during retirement, plus the potential for your property to appreciate over time.

How Can You Enhance Your Retirement Savings?

Looking to amp up your retirement savings? Here are a few tips:

- Maximize Contributions: Aim to make the most of your RRSP and TFSA contributions. For 2024, the RRSP limit is 18% of your previous year’s income, capped at $30,780.

- Review and Adjust: Regularly checking in on your savings plan and investment portfolio is crucial. Life changes, like getting married or having kids, might mean it’s time to tweak your strategy.

If you’re eager to learn more about saving for retirement, be sure to explore our comprehensive Canadian Retirement Planning Guide for in-depth strategies tailored just for Canadians.

Conclusion

Trusting Trust Your Talent means believing in your abilities to plan effectively for your retirement. Taking proactive steps in your retirement planning can truly set you up for success. By implementing smart saving strategies, leveraging the comprehensive resources available through Trust Your Talent, and regularly reviewing your progress, you can confidently navigate your retirement journey.

For additional guidance on specific topics like retirement income, check out our average couple retirement income guide and our insights on how much money you need to retire in Canada to ensure you’re prepared for the years ahead!

How Much Money Do You Need to Retire in Canada?

Planning for retirement can seem overwhelming, especially when considering how much money you’ll need to retire comfortably in Canada. This guide will provide you with clear insights into the expenses you’ll face, potential income sources, and actionable steps to help you prepare financially for your retirement years.

Understanding Retirement Expenses

The first step in determining how much money you’ll need to retire is assessing your expected expenses. A widely accepted benchmark is to aim for 70% to 80% of your pre-retirement income to cover housing, healthcare, and day-to-day living costs. For instance, if your pre-retirement income is $75,000 per year, you should aim for an annual retirement income of approximately $52,500 to $60,000.

Major Retirement Expenses to Consider

Housing Costs:

- Mortgage or rent payments

- Property taxes

- Home insurance

- Maintenance and repair costs

Healthcare Costs:

- Prescription medications

- Private health insurance premiums

- Out-of-pocket medical expenses

Daily Living Expenses:

- Groceries

- Utilities

- Transportation costs

Leisure Activities:

- Travel and vacations

- Hobbies and entertainment

Contingency Fund:

- Emergency home repairs

- Unexpected medical expenses

By evaluating these factors, you’ll have a clearer picture of your future needs. For a detailed breakdown of potential costs, you can refer to our Retirement Planning Guide for Canadians. It’s essential to plan based on your personal needs to ensure a secure retirement.

How Much to Save for Retirement

One of the most common questions is, “How much money do I need to retire in Canada?” The answer depends on factors like lifestyle, location, and financial goals. A general rule of thumb suggests having at least $1 million saved by the time you retire. However, this number can vary significantly depending on where you live. For example, retiring in a large city like Toronto or Vancouver might require a larger retirement fund than living in a smaller town.

Government Benefits and Their Impact on Retirement Savings

Government programs such as the Canada Pension Plan (CPP) and Old Age Security (OAS) are essential components of retirement income in Canada. They can help supplement your savings and reduce the overall amount you need to set aside.

- Canada Pension Plan (CPP): The average monthly CPP payment is approximately $1,200.

- Old Age Security (OAS): Eligible seniors receive around $615 per month from OAS.

These government benefits play a vital role in your financial planning. To determine how much more you need to save, subtract these amounts from your estimated retirement expenses. This approach will give you a more accurate figure for your personal savings goals.

How Much Money is Required to Retire?

The question of how much money you need to retire is often more complex than a single number. To calculate your retirement savings goal, you should follow a systematic approach that includes your projected expenses and expected income sources.

Steps to Calculate Your Savings Target:

- Calculate Your Total Annual Expenses: Start with an estimate of your annual expenses during retirement, including housing, healthcare, and living costs.

- Determine Your Income Sources: Estimate how much you’ll receive from government benefits (like CPP and OAS), pensions, or part-time work.

- Subtract Your Income from Your Expenses: This will give you the annual shortfall you’ll need to cover with your personal savings.

- Calculate the Total Amount Needed: Multiply your annual shortfall by the number of years you expect to live in retirement. For example, if you have a $20,000 shortfall per year and expect to live 25 years in retirement, you will need $500,000 in savings to fill the gap.

For a more detailed method of determining your retirement needs, check out our article on calculating retirement income.

Recommended Retirement Savings by Age

Knowing how much to save at different stages of your life can help you stay on track for retirement. Financial experts recommend setting savings milestones to ensure you’re financially prepared when the time comes to retire.

Savings Targets by Age:

- By Age 30: Save at least 1x your salary.

- By Age 40: Target saving 3x your salary.

- By Age 50: Aim for 6x your salary.

- By Age 60: Save 10x your salary.

For example, if you earn $80,000 annually, by age 60, you should have around $800,000 saved. This savings goal provides a solid foundation for a comfortable retirement. If you’re looking for more information on retirement savings strategies at different life stages, check out our comprehensive guide on saving for retirement.

How Much Do You Need to Retire Comfortably?

Retiring comfortably means being able to maintain your current lifestyle without major adjustments. The amount you need to save will depend on how you want to live in retirement.

Tips for a Comfortable Retirement:

- Start Early: Begin saving as soon as possible to maximize the benefits of compound interest.

- Diversify Investments: Spread your investments across a mix of assets like stocks, bonds, and real estate to minimize risk.

- Review Regularly: Reassess your retirement savings plan annually and adjust based on changes in your financial situation.

- Seek Professional Guidance: Consult with a financial advisor to tailor your retirement strategy to your specific needs and goals.

For more details on ensuring a comfortable retirement, read our retirement planning strategies.

Conclusion

In summary, determining how much money you need to retire in Canada depends on several personal factors, including lifestyle, location, and income sources. While aiming for around $1 million in savings is a good starting point, you must consider your unique retirement goals and government benefits like CPP and OAS.

Trust Your Talent and take proactive steps to plan for your financial future. By leveraging expert advice and staying committed to your savings goals, you can secure a financially sound and enjoyable retirement. For more resources, explore our full Canadian Retirement Planning Guide and get expert insights to help you build a successful retirement plan.

Average Couple Retirement Income: What to Expect in Canada

Understanding the average couple’s retirement income in Canada is essential for effective retirement planning. With the cost of living constantly changing, knowing what to anticipate helps set realistic savings goals and informs financial decisions. This guide provides valuable insights into expected income levels, sources of income, and strategies for retirement planning.

What is the Average Retirement Income for Couples in Canada?

The average retirement income for couples in Canada is approximately $60,000 to $70,000 per year. However, this figure can vary based on several factors, including:

- Geographic location: Couples living in urban centers may face higher living costs than those in rural areas.

- Lifestyle choices: Individual preferences for travel, hobbies, and leisure activities will influence overall expenses.

- Health care costs: Anticipating potential medical expenses is crucial for accurate financial planning.

In addition to these factors, it’s important to consider how different sources of income contribute to your retirement funds. For a more in-depth understanding of how much money you need to retire, visit our guide on how much money you need to retire in Canada.

What Are the Main Sources of Retirement Income?

Most couples rely on a combination of sources for their retirement income. Understanding these sources can help you estimate your expected retirement income more accurately.

1. Government Benefits

Government benefits play a significant role in retirement income for Canadians. The two main programs are:

- Canada Pension Plan (CPP): The CPP provides a monthly pension to eligible Canadians based on their contributions during their working years. On average, couples can expect to receive about $1,200 to $1,800 per month from the CPP.

- Old Age Security (OAS): OAS is a universal pension plan available to all Canadians aged 65 and older, regardless of work history. The average OAS payment is approximately $615 per month.

Together, these government benefits can provide a crucial financial foundation for your retirement.

2. Personal Savings

Personal savings are vital to achieving a comfortable retirement. These savings typically include:

- Registered Retirement Savings Plans (RRSPs): RRSPs are tax-deferred accounts that encourage individuals to save for retirement. Contributions are tax-deductible, and investment income grows tax-free until withdrawal. Depending on your contributions and investment growth, your RRSP could provide a significant source of retirement income.

- Tax-Free Savings Accounts (TFSAs): TFSAs allow Canadians to save money tax-free. Unlike RRSPs, contributions to a TFSA are made with after-tax dollars. Any income earned within the account is not subject to tax, making it an attractive option for long-term savings.

For effective savings strategies and tips on maximizing your retirement funds, check our page on the best ways to save for retirement in Canada.

3. Pensions

Employer-sponsored pension plans can significantly enhance overall retirement income. There are two main types of pension plans:

- Defined Benefit Plans: These plans provide a guaranteed income based on a formula that considers salary and years of service. For example, a couple might receive a combined pension of $2,500 per month from their employer-sponsored plan.

- Defined Contribution Plans: In these plans, the retirement benefit depends on the contributions made and the investment performance of the account. While there is no guaranteed payout, individuals can build significant savings if they start early and contribute consistently.

How to Calculate Your Retirement Income Needs

To determine how much you need to save for a comfortable retirement, follow these steps:

- Estimate Your Annual Expenses: Aim for 70-80% of your pre-retirement income. This amount considers that some expenses, such as work-related costs, may decrease upon retirement.

- Factor in Government Benefits: Calculate expected CPP and OAS payments. The combined total will significantly influence your retirement income.

- Identify Your Income Sources: Include personal savings, pensions, and other potential income streams. For instance, if you have rental properties, this income should also be included in your calculations.

- Create a Comprehensive Plan: Use tools like retirement calculators to simulate different scenarios. For more detailed insights, refer to our Canadian retirement planning guide.

What is the Importance of Budgeting in Retirement?

Budgeting is critical for effective retirement planning. It helps you keep track of your income sources and expenses, ensuring you can maintain your desired lifestyle. Here are some steps to create a retirement budget:

- List Your Fixed Expenses: Include housing, utilities, insurance, and transportation costs.

- Estimate Variable Expenses: Consider travel, hobbies, and leisure activities.

- Plan for Unexpected Costs: Allocate funds for emergencies or unforeseen expenses, such as medical bills.

- Review and Adjust Regularly: Your budget should be a living document. Regularly review your income and expenses to make necessary adjustments.

How Can You Maximize Your Retirement Income?

- Start Saving Early: The sooner you start saving, the more time your money has to grow. Compound interest can significantly enhance your savings over time.

- Diversify Investments: Don’t put all your eggs in one basket. Diversifying your investments across various asset classes can reduce risk and improve returns.

- Utilize Tax-Advantaged Accounts: Take advantage of RRSPs and TFSAs to maximize your retirement savings while minimizing tax liabilities.

- Consider Delaying Retirement: Working a few extra years can boost your retirement savings and increase your CPP and OAS benefits.

- Review Investment Performance Regularly: Stay informed about your investments and adjust your portfolio as necessary to align with your risk tolerance and retirement goals.

Conclusion

Planning for retirement is more than just understanding the numbers—it’s about taking actionable steps to secure your future. By recognizing the average income couples can expect and the variety of income sources available, you can begin preparing effectively. With the right strategies in place, such as leveraging government benefits, building personal savings, and exploring employer-sponsored pensions, your path to a financially stable retirement becomes clearer.

At Trust Your Talent, we believe that empowering yourself with the right knowledge and resources is key to this success. Whether you’re just starting or looking to refine your retirement plan, our programs and upcoming events can help you navigate your financial future with confidence. Stay tuned for our upcoming workshops and webinars designed to guide you through every step of your retirement planning journey.

Frequently Asked Questions (FAQ)

What is the average retirement income for couples in Canada?

The average retirement income for couples in Canada is $60,000 to $70,000 per year, depending on lifestyle and location.

2. How much do I need to save for retirement in Canada?

You should aim to save 70% to 80% of your pre-retirement income to maintain comfort during retirement.

3. What are the main sources of retirement income in Canada?

Primary sources include Canada Pension Plan (CPP), Old Age Security (OAS), personal savings, and employer pensions.

4. What is the best way to save for retirement in Canada?

Contributing to RRSPs, TFSAs, and maintaining a diversified investment portfolio are top strategies.

5. How much does the average Canadian need to retire?

The average Canadian may need around $1 million in savings to ensure a comfortable retirement.

Canadian Retirement Planning: Your Complete Guide to Financial Security

Planning for retirement in Canada requires strategic thinking, financial goal setting, and a clear understanding of the components that contribute to a secure financial future. This guide will take you through everything you need to know about retirement planning in Canada, from government benefits to personal savings strategies.

Understanding Canadian Retirement Planning

Canadian retirement planning involves creating financial goals, saving, and investing to ensure a comfortable lifestyle after you stop working. The process takes into account several unique factors of the Canadian financial landscape.

Why Retirement Planning is Important in Canada

Retirement planning is vital in Canada for several reasons:

- Increased life expectancy: Canadians are living longer, with the average life expectancy reaching 82.66 years in 2021.

- Rising healthcare costs: Healthcare in retirement can be expensive, and costs continue to rise.

- Government benefit limitations: Future reductions in benefits are possible

- Financial independence: Ensuring you can maintain your standard of living in retirement is crucial.

Because Canadians are living longer, your retirement savings will need to last for an extended period.

Key Components of Canadian Retirement Planning

1. Government-Sponsored Plans

Canada provides government programs to help with retirement income:

- Canada Pension Plan (CPP): Contributory plan based on your work history.

- Old Age Security (OAS): Monthly payments for those 65+.

- Guaranteed Income Supplement (GIS): Additional support for low-income seniors.

As of 2023, the maximum monthly CPP payment at age 65 is $1,306.57 .

2. Employer-Sponsored Plans

Many employers in Canada offer retirement savings plans:

- Registered Pension Plans (RPPs): Employer-contributed retirement savings.

- Group Registered Retirement Savings Plans (Group RRSPs): Voluntary contributions through payroll deductions.

3. Individual Savings Plans

Your personal savings are key to securing your retirement:

- Registered Retirement Savings Plans (RRSPs): Tax-deferred savings account.

- Tax-Free Savings Accounts (TFSAs): Tax-free savings and investment income.

- Registered Retirement Income Funds (RRIFs): Conversion of RRSPs into a steady income stream in retirement.

4. Non-Registered Investments

Non-registered investments can supplement your retirement income:

- Stocks and bonds: Higher risk, potentially higher return.

- Mutual funds: Professionally managed portfolios.

- Exchange-Traded Funds (ETFs): Low-cost, diversified investment options.

5. Real Estate Investments

Real estate can provide long-term financial security:

- Primary residence: Often a valuable asset for retirement.

- Rental properties: Generate passive income.

- Real Estate Investment Trusts (REITs): An alternative to direct property ownership.

Understanding Retirement Income in Canada

The median after-tax income for senior couples in Canada was $63,000 in 2019 . However, this number can vary based on individual situations.

Key questions:

- What is a good retirement income in Canada?

- How much do you need to retire as a couple in Canada?

For more on these, see our detailed guide on the average couple retirement income in Canada.

Determining Your Retirement Needs

The amount you need to retire depends on several factors:

- Desired lifestyle

- Expected lifespan

- Inflation and rising costs

- Healthcare expenses

- Current savings and investments

Key topics:

- How much money do I need to retire?

- How much should I save for retirement in Canada?

- RRSP amounts by age.

Check out our guide on how much you need to retire in Canada for detailed insights.

Effective Savings Strategies for Canadian Retirement

Saving for retirement in Canada requires a mix of strategies:

- Max out contributions to RRSPs and TFSAs.

- Utilize employer-sponsored retirement plans.

- Diversify investments to match your risk tolerance.

- Consider real estate as part of your portfolio.

Focus on:

- Retirement essentials

- Investment and savings strategies

- Best retirement plans in Canada

Our guide on the best way to save for retirement in Canada dives deeper into these strategies.

Calculating Your Retirement Needs

How Much Money Will You Need for Retirement

Calculating your retirement needs involves assessing:

- Desired retirement lifestyle

- Anticipated retirement age

- Expected lifespan

- Inflation and cost of living

- Healthcare expenses

Helpful tools:

- Early retirement calculators

- Retirement income assessments

- Goal planning guides

Conclusion: Securing Your Financial Future with Trust Your Talent

Planning for retirement in Canada means understanding your options, from government benefits to savings strategies. By starting early, staying informed, and regularly adjusting your plan, you can work towards a financially secure future.

At Trust Your Talent, we recognize that every retirement journey is different. Our expert financial advisors are here to help you navigate the complexities of Canadian retirement planning, offering personalized strategies to ensure you’re on the path to a comfortable retirement.

Frequently Asked Questions (FAQ)

What is the best age to start retirement planning in Canada?

It’s best to start as early as possible—ideally in your 20s. Starting early allows you to take advantage of compound interest, giving you more time to build a solid retirement fund.

How much should I save for retirement in Canada?

A common guideline is to save 10-15% of your income. However, the amount you should save depends on your desired retirement lifestyle and individual circumstances.

Can I retire early in Canada?

Yes, early retirement is possible, but it requires careful planning. You will need to consider reduced CPP benefits, a longer retirement period, and higher healthcare costs.

What happens to my RRSP when I retire?

You must convert your RRSP to an RRIF or buy an annuity by the end of the year you turn 71. RRIFs provide a steady income stream, and withdrawals are taxable.

How does the Canada Pension Plan (CPP) work?

The CPP is a contributory program based on your work history. Contributions are made throughout your working years, and benefits depend on your contributions and the age you start receiving them (standard age is 65).